I’ve been planning the move for several years, and I just pulled the trigger for the first time in my life. I plan on pulling that same trigger annually for the next 15 years, or until there’s a fundamental change in USA tax law. The trigger I pulled? A Before-Tax rollover into a Roth IRA. In my case, the before-tax money was in my 401(k). In your case, you may have before-tax money in an IRA. The same strategy applies whether your before-tax money is in a 401(k) or an IRA.

Earlier this month I executed my first before-tax rollover, and today I’m going to tell you why. I’ll also explain how I executed the trade with Vanguard in the event you’re considering doing the same. Given today’s favorable tax rates, it’s my opinion that now is a strategic time to consider taking some action to reduce your overall tax liability during retirement.

Why I just did a Before-Tax rollover into a Roth, and why you may want to consider doing the same. Click To Tweet

Why I Just Did A Before-Tax Rollover Into A Roth

It sure was nice saving money in my Before-Tax 401(k) account during my working years. All of the contributions were deducted from my pay for the year, and my current year’s tax liability was reduced accordingly.

Unfortunately, Uncle Sam isn’t as generous as he may appear. When it comes time to access that before-tax money in retirement, Uncle Sam comes calling for those taxes he let you avoid in your working years. He’ll not only tax your contributions, but he’ll also be staking his claim on any earnings those contributions have earned. Here’s a quick definition of both the before-tax and Roth accounts:

- Before-Tax IRA/401(k): Contributions are tax-deductible, earnings and contributions are taxed when withdrawn. Required Minimum Distributions will force withdrawals at Age 70 1/2+.

- Roth: Contributions are made with after-tax dollars, earnings and contributions are withdrawn tax-free. No Required Minimum Distributions apply.

Taxes are one of the major expenses we must manage in retirement and the tax expense associated with accessing our Before-Tax retirement savings can be significant. Any withdrawal from before-tax savings is treated as income in the year you make the withdrawal and taxed at your marginal tax rate. If you don’t withdrawal any of your money, you’ll be forced into withdrawals at Age 70 1/2 under the Required Minimum Distribution (RMD) laws of the IRS.

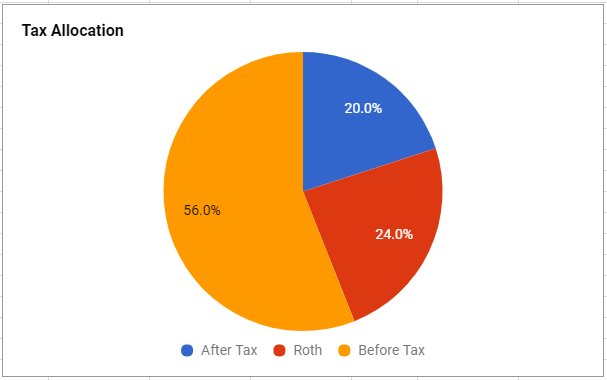

If you’re a babyboomer who has been saving through an employer’s 401(k) plan, or you’ve opened an IRA during your working years, chances are you have some investments in a before-tax account. Having too much in a before-tax account is one of the Top 7 Mistakes Retirees Make. I’m guilty of that sin with 56% of our retirement savings in before-tax accounts. When we were in the first half of our career, we didn’t have access to Roth’s, so before-tax savings made a lot of sense at the time.

The chart below comes from the article I wrote which explains Our Retirement Investment Drawdown Strategy, in which I first outlined our intention of using this before-tax rollover strategy. You’ll see the problem we’re facing, especially if we wait until RMD’s force us to begin withdrawing (and paying taxes on) that significant slice of before-tax savings:

Now that we’re in retirement, it’s time to correct the sins of our past. There is a strategy to minimize the lifelong tax bite from excessive before-tax savings that I strongly support. I’ll refer to it as the “Topping Off” Strategy, and it’s an approach I’m taking in our early retirement. Fortunately, I’m able to access my 401(k) without penalty since I retired at Age 55 (see 401k Age 55 rule), so I decided to go ahead and get started on executing my Topping Off Strategy this year. I suspect it may also make sense for you, though you will have to clearly understand your personal situation before finalizing any decisions. Be particularly careful if you’re eligible for ACA health care subsidies, or 0% Capital Gains, or Medicare subsidies, as the rollover will increase your income and may exclude you from those benefits.

In a nutshell, the “Topping Off Strategy” suggests that from the date you retire until you reach Age 70, you should consider “topping off” your current income tax bracket with annual withdrawals or rollovers from your Before-Tax accounts. These withdrawals will be taxed at your current marginal tax rate, which may be lower than the tax rate you’ll incur if you wait until the RMD law forces you to take heavier withdrawals in the future.

How To Use The “Topping Off” Strategy To Determine your Before-Tax Rollover Amount

Let’s work through an example of how to apply the strategy. The example will explain exactly how I used the strategy to execute our before-tax rollover, though the figures in the example are hypothetical to demonstrate the process.

First, take a look at the following graphic which explains the 2018 tax brackets for a “Married/Filing Jointly” couple from my article “The New Tax Law Loophole That Benefits Retirees” . (Note the chart was from 2018, but I’m using 2019 bracket levels in the example below. For the 12% tax bracket, the top of the bracket in 2019 has increased from $77,400 to $78,950. You can find the 2019 tax brackets here.)

Focus on the blue line and the “New Tax Law” box in the upper right-hand corner, we’ll be referencing those numbers in the example below. Also note how much lower the blue line is than the red line, reflecting the new tax laws implemented in 2018, and one of the reasons why I executed our rollover this year.

Now focus in on that 12% tax bracket, which covers income from $19,050 to $77,400 (again, we’ll use 2019’s revised top of $78,950 in the calculation below). If your income falls into a different tax bracket, the methodology is the same, which is summarized below. The first step is to estimate your net taxable income for the current year, including any deductions you plan on taking:

| Definition | Amount | Notes |

| Retirement Income | $65,000 | Pension, side hustle income, etc. |

| + Investment Income | + $10,000 | Dividends, etc. |

| – Standard Deduction | – $24,000 | Married filed jointly |

| – HSA Contribution | – $8,000 | HSA’s are deductible |

| = Net Taxable Income | $43,000 |

Once you’ve estimated your net taxable income, you simply subtract that amount from the “top” of your current income bracket. In this case, you’d subtract the $43,000 taxable income from the $78,959 “top” of the 2019 bracket to determine a before-tax rollover amount of $35,950. ($78,950 – $43,000 = $35,950)

I would strongly recommend that you contact your CPA before you take the next step. In my case, I shared my calculation with my CPA and explained what I was planning to do. She immediately understood, double-checked my assumptions, and confirmed that my target rollover amount was appropriate.

BE CAREFUL if you currently qualify for ACA subsidies. Executing a before-tax rollover will increase your taxable income, and may result in the sacrifice of your subsidy. If you’re receiving an ACA subsidy (see income ranges in this post from Financial Samurai), I suspect you’ll find that doing a before-tax rollover is NOT in your best interest. Also, as stated above, beware if you’re eligible for 0% Capital Gains, which tops out at $78,750 in 2019 for folks who are married, filing jointly. If you’re over age 65 and on Medicare, beware if you’re currently eligible for subsidies. It’s very important that you understand the details of your personal situation before deciding on whether or not to implement the before-tax rollover strategy.

So, back to our example. Now we know that $35,950 is your targeted before-tax rollover amount. For simplicity’s sake, I’d suggest you round the target down to $35,000. I prefer to keep a bit of a buffer between the before-tax rollover amount and the top of your current tax bracket, just in case some of your assumptions turn out to be slightly different than your actual year-end figures.

The next step is to implement the trade.

Executing The Before-Tax Rollover With Vanguard

Once I had identified the amount I wanted to rollover to “top off” our tax bracket, I called Vanguard’s Participant Services @ (800) 523-1188 to execute the trade. In the case of my employer’s 401(k), a before-tax rollover cannot be executed online, so a call is required. I suspect the same is true for most plans.

The Vanguard representative was familiar with what I was planning to do, and it was a straightforward discussion on the steps required. The Vanguard rep filled out some paperwork to reflect the withdrawal from my previous employer’s 401(k) plan and rollover into my (existing) personal Roth IRA. If you’ve not yet established a personal Roth IRA, you’ll need to do this simple step in conjunction with your rollover. You could roll it over into a Roth in your 401(k), if available, but I wouldn’t recommend this option. Roth money in a 401(k) is subject to RMD’s, whereas Roth money in a personal account is not (at least under current tax law, subject to change…).

One shortcoming: In my plan, I cannot identify specific funds to sell for the withdrawal. Rather, the withdrawal is done a percentage basis from all of my 401(k) holdings. I was able to dictate which funds I wanted to purchase when the rollover moved to my Roth IRA, and I directed the Vanguard rep to buy the following:

- Small Cap Value (VSIAX) 50%

- International Fund (VTIAX) 25%

- 500 Index (VFIAX) 25%

Since I consider these Roth funds to be part of my “Bucket 3” in the Retirement Bucket Strategy, I elected to invest them entirely in stocks. Since I knew that I needed to increase my stock allocation slightly to achieve my Targeted Asset Allocation, I was comfortable taking some of the bond allocation from my before-tax 401(k) account and reallocating it to equities as part of the rollover trade.

An important consideration is the fact that Vanguard does not withhold taxes on the withdrawal from the before-tax account (remember this amount will count as income in the current year and will be taxed at your marginal tax rate). I’m not sure if this is always the case or rather a specific detail of how our retirement plan works. If your before-tax rollover is a significant amount, you’ll want to talk to your CPA about processing an estimated tax payment in the current calendar year to ensure you don’t get penalized for under-paying your taxes during the year. In our example, the before-tax rollover will generate a tax bill of $4,200, which reflects the $35k rollover amount X 12% marginal tax rate ($35,000 X 12% = $4,200). In my case, I’ve been paying estimated taxes each quarter and had built in an assumed before-tax rollover in my initial calculation, so I was comfortable that I was sufficiently covered.

A few days after my call I received the paperwork from Vanguard via snail mail, reviewed the planned before-tax rollover details, filled in the details on the Roth IRA funds I wanted to purchase, signed the document, and mailed it back to Vanguard.

A few days later the trade was executed, and I reviewed the details in my “transactions” screen on Vanguard.com to confirm everything had occurred as planned.

I had just completed my first-ever Before-Tax Rollover into a Roth!

Benefits Of A Before-Tax Rollover Into A Roth

The money that I rolled over will now be able to grow tax-free for the rest of my life. I was also able to reduce my future RMD liability while knowing the marginal tax rate I was paying on the current rollover. I view the move as a diversification strategy, paying a bit of the tax at a known rate now while reducing my future tax obligation (at an unknown, but possibly higher rate, later). I also feel rather strongly that the current tax rates present a good opportunity, given that the current brackets are favorable compared to historical ranges, and there is a high probability future tax rates will increase to offset the growing government shortfalls. That’s merely my opinion, but it’s a consideration if you happen to share my point of view. Finally, I was also able to make a small adjustment in my asset allocation during the rollover, which helps keep me on track with my targeted asset allocation.

Shortcomings Of Executing The Trade With Vanguard

I prefer to do any trades immediately, and online. It’s annoying to me that a phone call is required, forms are snail-mailed out to me, and then have to be snail-mailed back to Vanguard. Given the long-term nature of a before-tax rollover strategy, it’s not a trade you should attempt to “time”, but it’s a bit nerve-wracking to wait several weeks for the trade to be finalized. Also, the inability to target specific funds on the “sell” side from my before-tax 401(k) account limits my ability to be selective in what I choose to sell. Again, given the long-term nature of this trade, those are shortcomings I can live with.

Conclusion

We should all seek ways to minimize our expenses in retirement, and focusing on tax minimization for our before-tax investments is important, especially if you’re carrying a large balance in your before-tax accounts. If you have room in your current tax bracket, I encourage you to consider following my example and executing a before-tax rollover before the end of the calendar year (unless you receive ACA subsidies or are close to the 0% Capital Gains cap, and in all cases never without reviewing your personal details with your CPA or other qualified professional).

If nothing else, have a phone call with your CPA and see if the strategy might be worth considering in your situation. If you’d prefer to be more aggressive, you can also rollover money to the top of your next higher tax bracket, though this would be a much larger rollover amount and shouldn’t be done without firmly understanding your strategy. Don’t procrastinate if you decide to implement the strategy this year, it took me almost a month to execute my trade and the trade will need to be executed before December 31st.

Your Turn: Have you ever executed a before-tax rollover? Do you agree that the “Topping Off” strategy is worth considering for any retiree with a sizeable balance in their before-tax accounts? Are you worried about the impact of your RMD’s when you turn 70 1/2? Finally, am I missing anything in my strategy? Let’s chat in the comments…

Given that you are executing both the sell (from 401k) and the buy (in the Roth IRA) with Vanguard, are the two batches of transactions executed on the same/next day or is there a bigger gap between selling and buying? I ask because if there is a bigger gap this introduces yet another issue to be considered.

Good question, Al. I was also curious how it would be executed, turns out that both the “buy” and the “sell” legs were executed with the closing prices on the same day. I agree that a gap between the buy and the sell would increase the timing risk of the trade.

Thanks for the article. I am surprised Vanguard doesn’t allow an in-kind conversion. TDAmeritrade does. I will definitely convert I kind IRA stock shares to my Roth.

Etrade allows in kind conversions also, at least with IRA to Roth IRA.

Janice, I believe the constraint is the 401(k) requirements of my employers plan, not a specific Vanguard limitation. For example, I believe a simple in-kind conversion can be done between a Vanguard before-tax IRA and a Vanguard Roth. That said, the conversion from my Vanguard 401(k) to Vanguard Roth was, in effect, an “in kind” conversion since no check was issued to me, the assets simply rolled directly over to the funds I selected.

Fritz, what would the pros/cons be of rolling over your entire 401(k) to your traditional IRA and then all future Roth conversions would be IRA-to-IRA without your employer’s 401(k) rules/limitations?

Certainly an option, Eric. I’d have to do some research to ensure I could still access my before-tax money if I move it to an IRA (I’m currently using the Age 55 rule to access my 401(k), since I retired at age 55), would hate to lose the years until age 59 1/2. Also, my 401(k) has an attractive fixed income option (using GLIC’s) which isn’t available in “normal” Vanguard funds, so I haven’t been in a hurry to leave my 401(k). Finally, my 401(k) is with Vanguard, so I’m happy with the expenses and fund availability. The benefit of rolling it into an IRA would be the ability to do my once-per-year ROTH rollover with the click of a mouse.

The 55 rule only applies to your employer plan. The IRS rule is specific about this. So don’t roll any funds out of your 401K that you will need for your age period between 55 & 59.5 years.

I love it! Thank you, Fritz. Seeing the nuts and bolts of an actual 401(k) to Roth conversion was very educational. The top-off strategy is financial gold. I’m going to run the numbers again, but I don’t think the strategy will work for us. Mrs. Groovy and I are ACA moochers, so the effective tax rate on our rollover will probably be too high. I think the last time I ran the numbers, the effective tax rate was close to 50 percent. Sigh. But at least we’ll know what to do when we’re both on Medicare and have three years to do non-ACA-influenced rollovers. Great freakin’ post, my friend.

I was thinking of you when I added that ACA dislaimer, Mr. G. Clearly, the costs of losing that ACA subsidy would lead to a different decision than the one made by those of us who don’t get the ACA subsidy. You’re a lucky man, take it for as long as you’re able!

The Medicare income buckets become more critical for us (slightly) older folks as $1 over each income level raises your entire Medicare cost while income taxes only raise for the incremental over the the income threshold. I find that planning my Roth conversions are more about the Medicare income limits than the income tax buckets (but YMMV).

This post was very timely for me as I just completed my first Roth IRA conversion this year. I’m the same age as you Fritz and my husband and I also have a large percentage of pre tax investments. I’m also planning to do Roth IRA conversions until we reach age 70.5. The other advantage of Roth’s is that it will keep the surviving spouse in a lower tax bracket too.

I agree 100%, Paul, hence my warning for those of you who get Medicare cost breaks based on income thresholds. I’m not there yet, but I understand going above those thresholds can be very punitive. Thanks for providing a real life example!

I did Roth conversions from retiring at 55 til 63 to avoid the high taxes on RMDs I would have incurred. Medicare looks back two years to determine if you go over income limits requiring you to pay higher medicare premiums. For singles it is 85K. So be sure to check that before doing Roth conversions after 63.

Thanks for teaching me something today, Mel. I wasn’t aware of the two year “look back”. Thanks for the great addition to the conversation!

I suspect you have a reason why you have not rolled over your 401(k) to an IRA. Between my wife and I we had 3 401(k)s and rolled them all into our Vanguard accounts. This should make the partial Roth conversions that we plan to do starting in a couple of years more efficient than your experience I would think. The partial Roth conversion strategy also fits nicely in an overall plan if you are delaying SS. Also it is good to have the cash outside your retirement accounts to pay the taxes so you are not “double-taxed” on the withdrawal. I am also hoping the Secure Act passes which will give me a couple of more years (70.5-72) to do partial Roth conversions. The other thing I would say about this is that should be more emphasis on tax diversification during the working years so there is more balance between taxable, tax-deferred and Roth accounts in retirement-at some point stuffing nearly everything into a tax-deferred account may not make sense, depending on income levels.

Could be because of the 59 1/2 rule. If you leave your employer after 59 1/2, you can withdraw from the 401k without penalty. Even though Fritz retired before 59 1/2, leaving that bucket alone would allow moving it to a future 401k after 59 1/2, easier. (The starbucks strategy; named because starbucks allows even part time employees access to the 401k) (Though, I’m not a tax lawyer)

Ah, actually I think it is Rule of 55 (which includes a 59.5 reference just for IRS “clarity”) . A rollover to IRA is allowed but if a withdrawal is taken from the IRA (including a withdrawal for a partial Roth conversion), before 59.5, a 10 % penalty applies. Good reason to tolerate the phone call and snail mail I guess.

Rob, with the Rule of 55, I could easily roll over my 401(k) to an IRA. The primary reason I’m not is that my 401(k), which is also with Vanguard, offers a very attracive fixed income fund that isn’t available in “normal” Vanguard funds. Were I to move to a Vanguard IRA, I’d lose access to that fund. Also, I think you’re correct that if I were to roll-over my 401(k) to an individual IRA, I’d lose the ability to do these before-tax rollovers until I’m age 59 1/2.

I’ll deal with the slightly more burdensome method of Before-Tax rollover for now, but at some point I will likely go ahead and roll over the 401(k). I’ll definitely do it before Age 70 1/2, since any ROTH’s in a 401(k) are forced into withdrawals by RMDs, whereas any ROTH in an individual IRA are not subject to the RMD requirement. Strange.

You can do a partial roll over of half your 401k money to an IRA and leave your living expenses in your 401k so you have access to withdrawls. Then you can manage your conversions in kind between ira & Roth while investing in the funds/stocks you want without limitations the 401k account holds you too. I know fidelity lets you do partials while under 59 1/2.

Just a quick clarification on your first paragraph: Rollovers from Traditional IRA’s or 401K’s to Roth IRA’s before 59 1/2 are allowed. Withdrawals are subject to a 10% penalty. So your strategy would still work if you rolled your 401K over to a traditional IRA before 59 1/2.

I am converting a very small amount this year (my first without work income) even though i-ORP tells me it is a wash whether I convert now or wait. Singles tax brackets ratchet up very quickly, so we singles are hitting the 22% bracket with only $39500 in income.

Thank you for the great article Fritz! For those of us working toward retirement would you suggest we allocate more to the Roth 401K? I am 50 and in my highest earning years. I am loving the tax break I get from putting my 17% toward before tax 401K saving but know the tax man will collect in the future. What would your advice be to me in my phase of accumulation? I also have 3% going to after tax account with an auto conversion to a Roth.

I’m curious about this too!

That’s a very difficult question, Linda, to which I totally relate. In my final years of work, I did increase my ROTH contributions (and reduced my before-tax contributions) even though it wasn’t necessarily “optimal” from a tax bracket perspective. I KNEW I had way too much money in before-tax, and decided to go ahead and do something about it with my final few years of contributions. Theoretically, you should only do ROTH until it triggers you into the next higher tax bracket. So, I’d look at your marginal income situation to make the decision on contributions. You also need to think about your income in retirement, and how feasible before-tax rollovers are going to be for you. Complicated subject, but you’re asking the right question!

Good post, Fritz. Another strategy once you turn 70 1/2 is to use a portion of the RMD from IRAs or 401(k) plans to fund church and charitable donations. Under current law, IRA charitable rollovers are not taxable. It makes sense at that point to stop writing checks and make all donations using the RMD.

Great addition to the post, Dave. I was aware of that feature, and plan on using it when I hit my 70’s if it’s still allowed. Until then, I’m using Donor Advised Funds and “lumping” several years of charitable donations every 3rd or 4th year.

Thanks for adding it to the discussion, great point that folks should be aware of if they’re living in the world of RMD’s.

I’ve been eying the same thing but as a brand spanking new retiree I’m haunted by sequence of returns given the current state of the market. The thought of spending more now (paying the taxes) to save later has me a bit spooked. I’m sure there is a mathematical way to figure it out more or less but I’ll be darned if I can get my arms around it! Great food for thought!

If you’re nervous, just convert part of what you could. It isn’t an all or nothing proposition. Good luck.

John, it’s certainly a challenge, since there’s no way to know what our tax rate will be “later”. I second the comment made by Steve Brown to consider doing a partial rollover, if that’s what you’re more comfortable with. I’m a big fan of diversifying our risks, and I feel rolling some of the before-tax over now, under known (and historically low) tax rates is a wise diversification move. Only time will tell whether it was the right move…

Hi I really liked your article. It is very helpful to see this information for retirement tax planning. A question and a comment. On the tax rate you mention in the example you pay the marginal tax rate on the Roth conversion amount. In the example case 12%. What if income is lower and some of the standard deduction covers the roll over. Do you still pay the marginal rate on the conversion amount or the reduced rate on the after deduction amounts?

Also in the example section you mention …”which tops out at $78,750…” should this be 78950?

thanks

Bruce, the marginal tax rate applies on any rollover amount. The amount you can rollover in the tax bracket is impacted by the amount of your standard deduction, as I attempted to show in the formula within the post. By deducting the $24k standard deduction, you can rollover a $24k higher amount than you’d be able to do without the deduction, trust that’s clear.

And yes, $78,950 is the 2019 top of the 12% bracket, apologies for the typo.

I have executed conversions from my IRA to my Roth Ira for 2 years online at Vanguard. I am able to convert in kind and just move shares from one account to the other. It may be the complications of your own 401K that is keeping this from being an easy transaction.

Thanks for confirming that the “burden” is 100% due to my employer 401(k) protocol, Dan. Good to know it’s easy to do an online rollover from a Vanguard IRA.

This is probably the subject matter I have most identified with since subscribing to your blog. Like you, Roth hasn’t always been an option for me, so most of my money is pre-tax.

I’m converting my IRA to a Roth now and will continue until that is 100% Roth. I’m taking a different approach with my 401k assets, however. My plan is to roll over the Roth 401k assets upon retirement while drawing from traditional 401k until 59.5. Then I’ll roll over the traditional assets to VG and begin converting that. For me, the hassle will be where I do the rollovers. Converting a traditional IRA to a Roth IRA once everything is at VG is a snap.

Glad to hear today’s post hit a chord with you, Steve! Your plan is certainly a viable approach and accomplishes the same end goal, without the hassle I have to deal with in rollovers from my 401(k) due to my employer protocols. I considered rolling over my entire 401(k) to individual IRA, but I like the fixed income choice which is only available in my 401(k), a GIC with a favorable interest rate. Also, I have access to my 401(k) between Age 55-59, whereas I believe I’d have to wait until Age 59 1/2 to do rollovers if I moved my 401(k) money into an individual IRA.

It is my understanding that you can convert funds in a rollover IRA to a Roth IRA before age 59.5 without penalty. Been doing it for several years directly online at Vanguard. Direct conversions have no penalty, but you cannot withdraw Roth funds until they are “seasoned” for 5 years. Withdraw Roth funds before then, and there is a 10% penalty. I think the main benefit from your 401k is that like many other 401k plans out there, you can withdraw from it for ANY purpose without penalty since you left work after age 55. That is nice security, and you would lose that if you did a conversion to an IRA, but you would still be able to do Roth conversions without penalty before 59.5 if you did convert the 401k to an IRA.

Good to know, Lisa. I love it when a reader teaches me something new! In fairness, I haven’t really researched it given that I’m happy with my 401(k) and the funds available. May have to consider it before I do my 2020 rollover!

The five year seasoning is from Jan 1st of the year you do the first Roth conversion so your five year count down Fritz for this October Roth conversion started Jan 1, 2019. 😁 But I think after 59.5 this five year rule no longer applies. Lara

Thanks, Fritz. A couple of questions. If you’re doing a rollover from an IRA, you can specify which fund(s) you want to withdraw the money from, correct? Also, in your example you have $10,000 of investment income shown as dividends…aren’t most dividends qualified dividends, in which case they’re taxed differently, and not as ordinary income? If you have qualified dividends, you wouldn’t include that amount in figuring your net taxable income, correct?

Thanks again for the article – I plan to do this also (once I’m retired)

While qualified dividends and long-term capital gains are taxed differently (at 0% if they fall within the 12% bracket) they do count toward filling up the 12% tax bracket.

I was not aware of that – thanks for the clarification.

Jennifer

Thanks for jumping in before I could get online, Mark. As for your first question, Jennifer, I am unable to specify which fund I want to withdraw money from due to the protocol of how my employer set up the 401(k). The withdrawal is pulled on a % basis from all of my holdings, and I’m unable to change it. That limit is driven entirely from the way my employer set up the 401(k). If you’re pulling from an individual before-tax IRA, you would be able to select the specific funds you want to withdraw money from.

Nice logically flowing post Fritz on how to convert to a Roth, tax efficiently. This year is my first rollover as well now that I am retired. My wife will still work for about 7-8 years. Her modest school social worker salary coupled with her maxing out her 403B and pretax healthcare benefits greatly reduces her taxable income. I have one more qualified deduction in alimony payments which further reduces our taxable income albeit for three more years. I am fortune to have significant non-retirement assets to live off before the RMDs which I will greatly reduce using this strategy. I only liquidate LT gains to keep that tax at zero. Like you, I am heavily skewed toward pretax retirement accounts, namely my traditional IRA since I transferred 401Ks & 403Bs along my career path. I have set up Vanguard to do these rollovers. Rather easy. I am curious as to why you selected your allocation for your third bucket?

Eduardo, I target my ROTH funds as bucket 3 since I’m planning to have these be the last funds I access (maximize that tax free growth for as long as possible). I have sufficient funds in my after-tax investments to cover Bucket 1 and most of Bucket 2. I’ll be using withdrawals from my Before-Tax to cover the balance of Bucket 2, when required. Therefore, I’m hoping to dedicate the ROTH money to Bucket 3 with 100% equity allocation. Trust that makes sense. Thanks for your frequent comments on my blog, I always appreciate what you have to say!

Fritz-Great post and discussion. I also have targeted my Roth (and associated conversions) as Bucket #3 money. But thinking about life after 59.5 (few years out still) I think a Roth account becomes a great Bucket #1 place-holder for money as well. It will allow for better control from a tax perspective (i.e., no unwanted dividends or interest that might get thrown off from a standard after-tax investment account). Ultimately, I envision pre-tax money flowing to Roth flowing to yearly spending account. All money stays in non-taxable (401k or Roth) account until needed. Of course, the investments within those accounts are Bucket #1, Bucket #2, and Bucket #3 type investments. All with the goal of simplifying the finance side of retirement!

Mark, good point about potentially utilizing Roth as Bucket #1 to better control taxes. Used in coordination with a before-tax rollover strategy could be of value to achive the targeted taxable income in a given year. Thanks for raising the point.

I have been implementing this strategy since retiring 3 years ago – – in no small part because of following financial bloggers like Fritz. As I analyzed my taxable income in future years, especially because my pension wasn’t going to kick in until age 65 and I plan to delay Soc Sec until age 70.5, it made infinite sense to me to pay more taxes now in my “leaner” years. I did roll my 401k to Vanguard when I retired and doing in-kind IRA -> Roth conversions really has been easy online. As I take taxable IRA withdrawals now to live on, I instruct Vanguard to withhold extra taxes to cover my annual tax liability by using a spreadsheet to keep track of my estimated taxes owed and paid in. This seems easier to me than submitting quarterly estimated taxes to Uncle Sam, but accomplishes the same thing. A big thank you to all of you who share your knowledge and expertise!

Mary, thanks for confirming that Vanguard IRA -> Vanguard ROTh conversion are easily completed online. We all now know the “complexity/burden” of my trade is 100% attributable to my employer protocol!

when doing these conversions, are there any unique things to do when filing taxes? is there another form? how is it entered? thanks.

The pre-tax portion of a Roth conversion is similar to an IRA distribution and is taxed as ordinary income. Form 1099-R reports the “distribution” for the conversion. Form 5498 reports the “deposit” into Roth.

If any IRA had after-tax basis, e.g., non-deductible taxes, you’ll file a Form 8606 that determines the taxable amount of the conversion and a new basis carried over on next year’s Form 8606.

IRS Instructions for Forms 1099-R and 5498

should be “non-deductible contributions”.

Dave, thanks for jumping in again with solid answers. Gees, you even included a link to the IRS instructions! Much appreciated!

The example rounded $35,950 of space in 12% bracket down to $35,000 for simplicity and to keep a buffer in case assumptions turn out to be slightly different than your actual year-end figures.

Not rounding down and converting additional $450 in next bracket (22%) isn’t a big deal since it’s only additional $45 in federal taxes. Most articles on Roth conversions suggest filling out a bracket. However, it might be worth converting into some or all of next bracket. For example, if you expect to have large RMD’s even after many years of converting $35K / year, today’s 22% bracket might be lower than your RMD bracket.

Correction to my comment: $450 should be $950, and $45 taxes should be $95 in taxes.

Glad to see I’m not the only one who makes the occassional mistake. Smiles.

And, for the record, I agree that having some fall “up” into the next tax bracket isn’t a bad move, depending on your circumstance. If, for example, you’re at the top of the 22% bracket, it may be worth considering “topping off” all the way to the top of the 24% bracket! Wow, that’d be a Mega Rollover…

Fritz, another wonderful article thank you. Ok so I am 69 1/2 so is there anything I can do ? I have to do the RMD in 2020 because my birthday is June 30th, wish it was July 1st. Any suggestions

JJ, thanks for the kind words. While there’s nothing you can do in 2020 and beyond, you can still take advantage of the “topping off strategy” for 2019, just make sure you get it completed by Dec 31, 2019. Also, for 2020 you should take note of the comment earlier in this “stream” about the option of using your RMD for charitable donations. Something to consider.

JJ, you can’t convert the RMD amount but depending on your income you can still convert additional withdrawals to top the tax bracket if you have room. Beware of the Medicare limitations of having to pay more in Medicare supplement premiums, it’s about $2,000 less then the tax bracket for singles.

Another great and timely article! I have about a 60/40 split between pre tax (401K, 403b) and Roth accounts with very little in taxable accounts. I plan on using the same strategy for next year because I just retired at the age of 52 and want to max out the 12% bracket before it expires in 2025 or is changed by Congress. I plan on drawing down my Roth accounts contributions over the next five years while converting 401K to Roth. I’m doing everything I can to avoid the 10% penalty because I left my employer before 55 and I’m also exploring a 72T withdrawal. I have a great CPA who will work with me on the tax strategy because it is a bit complicated. I believe I can get away from quarterly tax payments if I have a single conversion and pull taxes then. My ultimate goal is to have all my pre tax converted to Roth before hitting age 69 to avoid ever paying RMDs. Thanks again for sharing your journey!

Tom, a 72T is a viable option, though you’re definitely wise to confirm the (complicated) details with your CPA. I know once you start the 72T you must continue it on an equal basis, so it’s important to triple check all of the details before you initiate your first withdrawal/rollover.

And yes, you can avoid quarterly taxes if your only tax obligation is due to your rollover. The IRS allows a one time tax payment on the conversion, whereas any other income must have taxes paid on an approximately equal basis throughout the year.

One small edit Fritz – “If you don’t withdrawal any of your money, you’ll be forced into withdrawals at Age 70 1/2 under the Required Minimum Distribution (RMD) laws of the IRS.” You get the benefit of taking RMDs as long as you have a pre-tax balance, even if you have withdrawn some of your money :).

I appreciate the clear post. I’m also looking to complete my rollovers by age 63 (subject to change) to avoid medicare surcharges. I’m only 51% pre-tax, so balance is not too out of whack.

I’m retiring in the spring (59), but will likely delay any rollovers to 2021 so we are clear of the CA 9.3% marginal rate… It’d be a super win if we moved to Florida, but is a minor win just about anywhere.

Of course, you’re correct KevG. Thanks for clarifying this important point. Yes, you’ll still be forced into RMD’s at age 70 1/2 on any before-tax money. Hopefully, the burden will be lightened by some strategic rollovers prior to that age! Good luck on crossing The Starting Line and getting the heck out of tax-heavy CA! Wink.

Tax bracket arbitrage! Been doing it for several years. You correctly identified the caveats of capital gains (the “bump” – see excellent article written by Kitces), ACA subsidies and Medicare premiums. Each situation is different and your tax pro is a great place to start and/or review calculations.

I am surprised no one discussed or mentioned computing the IRR of the move. You are “pre-paying income tax sooner than necessary (investment) in order to pay less in the future (return). Prepaying taxes at age 55 (10-15 years in advance) to save taxes after age 70 may no be financially a great return. Alos, why stop at the top of the current tax bracket? The IRR calc is a little complex, but doable (multi-year tax estimate) and will guide you to determine how far to go.

One note — for your diligence, you will now be labeled a wealthy citizen who can afford to take advantage of “loopholes.” It happened to me.

RE: IRR point –

1) whatever return that, if no conversion was done for those 10-15 years, you would have this extra $ growth in the tIRA, so the taxes paid later on this bigger tIRA would obviously increase (*perhaps at a higher marginal rate too) due to this growth of that never-paid-earlier tax offsetting the time-value (‘IRR’) of the saved tax money, so I’m not sure that IRR would improve anyway and

2) I agree with Fritz’s educated guesstimation that tax rates will (absolutely!) increase after 2025 due to economic and political realities; thus pay now (Roth conversions) /save later. It’s all about tax bracket arbitrage (unless, as already pointed out, Medicare increases offset this, or 3.8% NIIT (tax on investment income at higher levels)or a negative effect on ACA subsidies). Good software or CPA needed ultimately.

Nice addition with the point about IRR. I see others have jumped in with some resources on that front, great point to add to the discussion. As for being “labeled”, I guess that’s the risk we take when we decide to blog publically about money! I’ll take my chances, there are worse things to be labeled as, right?

The standard deduction for married filling jointly increased from $24,000 to $24,400 in 2019.

There is an additional deduction of $1,300 if over 65 or blind.

Individual standard deduction increased from $12,000 to $12,200.

For single if over 65 or blind the additional deduction is $1,650.

Traditional IRA to Roth IRA conversions are taxable but not penalized prior to 59 1/2.

However, withdrawals may be penalized if draw before 59 1/2.

Good point about the increase in standard deduction, thanks for the correction (and addition of other important details).

I know four very good reasons that you have not emphasized in your article that should be considered.

1.First becoming a widow going down to single tax brackets – Decreases dramatically how much you can top off and so less cheaper Roth conversions. Do it now while you can take advantage of marriage tax brackets.

2. As a widow you can tap SS at 60 and Roth withdraws are not figured into the SS worksheet for SS taxability. You get to keep more of the SS income.

3. A combination of RMDs, SS , pensions and tapping Roth accounts can be very beneficial to lowering the amount of SS that is taxable thus dramatically lowering overall taxes and increasing overall yearly income. Starting Roth conversions in my 50s began a wonderful income stream -their earnings could conceivably pay All the taxes that I have to pay for all my Large tax deferred account balances if or when inflation causes my expenses to exceed my widow’s railroad retirement. Right now the taxes on my Roth Conversion are just a return on some of what I am getting from the government.

4. When considering Kevin S mention of IRR you would have to remember what you saved in your top marginal taxes and added company matches in 401k plans, (in my case 128-132% ) versus what amount of taxation you are paying at the top margin of taxes in the year of the conversion ( For me-Some12% and 22% -but and this is a big but-all paid from the check the government sends to me not out of my assets) . Sincerely, Lara

Excellent additions, Lara. I hadn’t thought about the reality that many older folks face becoming widows/widowers, and it’s clearly a strong reason to convert as much as possible while married/filing jointly. Same argument could be made about “Gray Divorce”, a concerning trend among Baby Boomers. Thanks for stopping by, your comments are always relevant and appreciated.

This is a great recap and thank you for mentioning the ACA issue(s). I specifically converted a small consulting gig to a remote work/benefits eligible gig to get into their corporate plan for 2020 and top out my Roth conversion.

I have a similar issue, sitting at 55%+ in tax deferred accounts plus some capital gain harvesting to do, these new tax rates are gold for early retirees for as long as they stock around.

SIS, great to see you stopping by! Congrats on swinging the remote work w benefits, nice! The tax rates are “gold”, best to take advantage of them for as long as they last (I don’t think they’ll last until I’m 70 1/2, for sure!).

Great post Fritz,

One item not mentioned by leaving funds in a 401K retirement account as opposed to a Traditional IRA has additional protective provisions in case you find yourself involved in a lawsuit. Employer-sponsored accounts are protected by the Employee Retirement Income Security Act. Your 30 day in kind transaction might not seem so bad.

I started the following 23-24 year project this year for my wife and I. It gave me a great excuse to get to column L on Excel. Row 84 is good until 2060. If I can still us a computer by then, I will be amazed. I shared the doc on Google Drive with my CPA. All I need to manually enter are EOY IRA Balance and EOY Roth Balance to ensure that we are both on the same page come tax time.

We chose to implement the Fixed Amortization Method:

Joint Life Expectancy Table

Reasonable interest rate: 3.06%

Substantially Equal Periodic Payments (SEPP)

Helpful RESOURCES, I have no affiliation with any link or website.

https://www.dinkytown.net/java/72t-calculator.html#

https://www.calcxml.com/calculators/roth-ira-conversion-calculator

https://financialmentor.com/calculator/roth-ira-calculator

Don’t forget to file Form 5329 (if necessary) to report the exception to avoid the 10% penalty if below 59 1/2.

https://www.irs.gov/publications/p590b#en_US_2018_publink1000231236

Ex’s.

Age 45 Ex. $205,000 ÷ 38.8 = $5,283.51 est. Tax $423

Age 46 $217,000 ÷ 37.9 = 5,725.59 est. Tax $497

Once the RMD’s start, turn off the auto reinvest dividends option in your 401K/ Traditional IRA and take the distributions into your brokerage MM account then transfer to your checking account to pay your quarterly taxes. No sense in exacerbating a situation that we are trying to avoid.

Also, consider a side hustle that you can barter your services or work a cash-based business during the holdfast stage of semi-retirement to keep your MAGI low. I am having trouble making my reported earned income of 7K this year so that I can contribute to my Roth. 😉

Scuba, great comment with specifics on 72T. Ironic you mention the lawsuit protection, I thought of that last night before I saw your comment when I was thinking about reasons to not move the 401(k) over to an individual IRA. I don’t expect to ever need that protection, but I think the value justifies the inconvenience of having to deal with the more burdensome process of doing the rollovers from the 401(k), I’m planning on keeping the $$ in the 401(k) for the time being. I’ll pretend I didn’t notice your comment about a “cash-based” business, wouldn’t want the IRS hitting you up on a tax audit… 😉

I also recognized the potential of this tax saving strategy a few years ago. In my mid-sixties, I started doing this last year with the intent to keep it up every year until RMD’s kick in. I started this year, with my planned amount in the beginning of the first two quarters, but am not continuing because we decided to sell a second home this year. Since it’s not a primary residence, we’ll have to declare the additional (capital gain) income, thus bumping us up in the bracket. We’ve got a couple more years to convert before I turn 70 1/2.

Paul, congrats on making an impact before you get burned by RMD’s. Congrats on the home sale, and on making some money on the sale. Smart move to skip a year of the ROTH conversions since you’re only facing a one year situation of being in the higher tax bracet. Well played.

I’m in my mid 30’s, new to FI, projected to reach FI in 10 years and I would like to (actually can’t wait to) retire a couple of years after that. Asset allocation is my recent topic of interest, among several different opinions out there, I was wondering what my trust worthy source (you) had to say about it. In doing so, I stumbled upon this article and I’m so glad! Because my assets are currently 95% in pre-tax… The general rule of thumb in FI community being ‘max out your 401k’, I was going back and forth between 401k and Roth 401k. After reading this article, I think I need to move towards Roth 401k. My husband and I started contributing to Roth IRA this year, opened a taxable account to survive the first 5 years of retirement until Roth conversion ladder kicks in. We’re currently in 12% tax bracket, with max-out contribution to HSA and Dependent care, I think we still will be in the 12% bracket without pre-tax 401k contribution. Does this sound alright?

Alee, congrats on discovering the path to FI while you’re still young enough to make a huge impact. At the 12% bracket, I would definitely encourage you to make ROTH contributions (as you get older, your income will likely increase and you’ll eventually move to higher tax brackets). You’ll have to do the math to figure out when you tip over the top of your bracket, but I would run the numbers and contribute to a ROTH at least until you top out of the 12% bracket. Kudo’s for being on top of this stuff, and thanks for stopping by!

My IRA is at Vanguard and I have done several IRA to Roth conversions. They were immediate, on-line, and from the funds I chose. The process went perfectly. Conversion with some 401Ks must use different rules.

Thanks for confirming, Tim. Makes sense that IRA to Roth (all at VG) would be a simple on-line move. I’ll deal with it for now, after age 59 1/2 I’ll likely move my 401(k) over to an IRA to simplify the annual rollovers.

Its amazing how similar our situations are. Im 56, worked at same company for 34 years, after meeting with Josh Scanlen I decided to retire in March. I have been following many financial blogs, reading and becoming as educated as possible. My husband and I each have pensions though not large..20k ea and his pension has lifetime medical coverage for us. 100% of our retirement savings is in 403b/401k. We are both planning on converting 75k each year before taking soc security at 67.

Although excited about the “green flag” to retire, Im still very, very nervous of giving up my high income job. Any advice?

Gina, amazing, indeed! Same age, started at same time, both know Josh Scanlen, both consume blogs and both have pensions. Wow! You’re fortunate to have lifetime medical through hubby’s employer, HUGE benefit as you prepare to cross The Starting Line in March.

As for your nerves, fear not. We all have a case of “the nerves” in our final months of work. Determine when “Enough Is Enough”, double check your math, make your decision and GO. Don’t look back. Think about what you want your life to be in retirement, and make it your focus for the next 4 months. Life is even better in retirement than I expected, I suspect you’ll find the same. Thanks for making me a small part of your journey. Enjoy your ride!

Great post Fritz! I’m planning on using this strategy next year which will be my first full year of retirement. As of now, I think I’ll need to wait until December to be able to estimate with any degree of certainty my dividend and capital gain income. Several of my funds pay annually in December and capital gains can fluctuate wildly from year to year. Love the “Top-off Strategy”!

I’ve gleaned much from your various posts. Thank you.

As a single guy, I’ve been preparing for possible early retirement myself, but may be a year or two behind your plan with not quite so much cushion. I too have heavily loaded my 401k over the years and will have my Roth funded to only about a tenth of what my 401k balance will be at the beginning of 2020.

My original plan was to start drawing distributions after separation of service from my employer and taking just what I needed for budgeted expenses while keeping the Roth for a cushion option if markets headed down too far to support my 4-5% planned withdraw rate. Given the historically low tax rates, it does seem to make sense to “Top Off” to max out the 12% marginal rate now.

I was surprised to read that your Vanguard plan did not withhold the standard 20% for Federal taxes. From what I’ve read in publications and retirement plan documents, 401k to Roth should trigger the automatic 20% withholding. Is it possible that they set up an intermediate traditional IRA and then moved it to the Roth.

If my plan (Securian Financial) has no way to stop the automatic 20% off-the top withholding process, it means I’m providing the Federal government with a huge interest free loan for the year since my real tax rate will be closer to half that. I don’t recall getting any significant tax refund in decades as I calculate my exemptions to ensure I pay a little each year.

Lane, I was surprised by Vanguard not withholding, as well. Everything I had read prior to doing my conversion said VG automatically holds them, but the VG rep said that’s not the procedure with my 401(k), and the entire amount was transferred (no taxes withheld). As for your question about whether they set up an intermediate traditional IRA, they did not. I could see the transaction on my VG screen, and it was directly transfered. Good to know, I’ll simply continue to include assumed ROTH conversions in my quarterly estimated tax calculations. Easy enough to do. Good luck on your journey, thanks for stopping by!

GOOD STUFF…. I’ve been rolling $ out of my IRA for a few yrs now since retiring; my 401K’s have all previously been rolled into my IRA. I either roll into my Roth or into my taxable account for my spending money the subsequent year.

I also manage my AGI, to continue to qualify for ACA subsidies (even with a 7 figure retirement portfolio). It’s not hard to do. Although some might think ‘it’s wrong’. 🙄

Just a reminder that going over the ACA threshold by even $1 will rid your complete subsidy and cost you about $20,00. YIKES!

As for staying within limits for $0 cap gains, which I also pay nothing, it’s not so penal if you go over the threshold. If you do happen to exceed, you only start paying the 15% on the amount of CGs that you go over, NOT your entire amount of cap gains.

Joe, nothing wrong with “managing your AGI”, you’re simply playing by the rules which have been provided, and there’s not a thing wrong with that! You’re “$1” comment is spot on, important stuff. Also, good add about the CapGains methodology. Thanks for adding to the discussion.

I’ve loved following you over the years Fritz.

I am lucky that I’ve been able to sock away a substantial amount in my Roth 401(k) but I have more money in my traditional 401(k) that might qualify for this strategy.

Just a pointer though, that just like affecting ACA subsidies, those people who are on Medicare might find that they are subject to IRMAA, and might have to pay more for Medicare Parts B and D if they go over the thresh-hold.

Kathe, great to see you leaving a comment on my site, thanks for being a long term reader (I love your podcast, too!). Great point about the Medicare, I did add two comments about that early on in the post, but didn’t include it in the Conclusion (and we all know most people just jump to the conclusion, in hindsite I should have added it there). Thanks for reiterating the important point of potential Medicare cost impacts.

Terrific post – and very timely as I was just discussing this topic with a friend this weekend. I’ve forwarded it on to him as additional food for thought!

One very minor question – I noticed in your hypothetical situation, you deduct the standard for married filing jointly and separately deduct an HSA contribution. Can you deduct an HSA if you aren’t itemizing? I didn’t know it could be deducted above and beyond a standard deduction and this will give me more room to convert traditional IRA money to Roth. 🙂

Thanks for the compliment, Sarah. Great question, and one I had myself. I found my answer on on this post from H&R Block, which states: “You are eligible for a tax deduction for contributions you made to your HSA even if you do not itemize your deductions.” I showed my calculation to my CPA and they agreed with it, so I trust the H&R Block statement is correct. You are correct in your statement that this allowance will “give you more room”. Thanks for stopping by!

Thanks for the swift reply and the link – I appreciate it!

There’s no question about it, the HSA contribution is an “above the line deduction” so you don’t have to itemize to get it on your federal return. However, not all states recognize the HSA as a deduction, so YMMV as far as state taxes.

Hey Nancy! I enjoyed your “goodbye” post to the NE, hope you’re enjoying the warmer southern weather as you’re reading my blog! I’m not as familiar with the 402(b), but I suspect it’s similar. Check the details with your plan provider, but I can’t imagine you wouldn’t be able to do Roth conversions. Thanks for stopping by!

Thanks for the swift reply and the link – I appreciate it!

The best information I receive in this post is that you can withdraw from 401K if you leave the job at 55 or later. That’s great news to me. Otherwise I would have to have a much bigger bridge account.

I like your 401K to Roth conversion strategy. But with a rental property (which will be paid for and generate about $17K annual net income by early 50), taking 4% from my 401K (about $30K annual) plus interest and dividend from other brokerage account, and filing as a single person, I am not sure if I can use the same strategy and not pay into the 22% tax bracket. Unless I sell the rental and convert home equity into stocks in my brokerage account and pull long term capital gains out to live on instead…

Thanks Fritz for the excellent article! I continue to struggle with this issue since I’m not in the 12% bracket. I’m 62, single, retired, in the 22% bracket (all passive income). Based on my calcs if I don’t convert I will still be in the same bracket range (although by then it will probably be at least 25% bracket) when I take RMD. That may not make sense at first glance, but a large part of my taxable portfolio is currently invested in a family business that pays me 6% interest, and in about 5 years that business will be sold and that money will be earning dividends on index funds (~2%). I do know that another factor in considering lowering RMDs is taxation of Social Security, but I’m subject to the WEP so my SS at 70 will only be about $600/mo. So I’m trying to decide whether to fill in the 22% bracket for the next 8 years (and pay 9.3% in state taxes on the conversions), or wait and see. I’ve consulted with a couple “professionals” and gotten completely different advice (1 for conversions and 1 against).

John, yours is a great example of why you really need to understand your individual situation before you make a decision. Sometimes, even the pros can’t agree! Sometimes, you just have to get to the point where you make a decision based on gut. Good luck with your decision, and thanks for stopping by.

Hi Fritz:

Back in February 2019 you were targeting moving $185,000 into a Roth conversion for 2019.

Fritz @ TheRetirementManifesto says:

February 7, 2019 at 11:43 am

Hi James! I had more income than expected in 2018, due to cashing in of some of my options, etc. at retirement. Therefore, I’ve decided to wait until 2019 to do my first Roth conversion. I’ll be moving ~$125k from my Before-Tax 401(k) into a Roth later this year.

Can you explain your strategy/thinking of going with $35,950 per this recent post ?

Many thanks

Best – James

James, I’m impressed with your organizational skills! If you read the post, you’ll see this statement: “The example will explain exactly how I used the strategy to execute our before-tax rollover, though the figures in the example are hypothetical to demonstrate the process.”

As you know, I don’t share our financial details on this blog (beyond asset allocation and percentages), and chose to go with a hypothetical example for this post to explain the process. I will say that the assumption I had when I sent you that email proved inaccurate, and I ended up converting a smaller amount to hit my targeted tax bracket ceiling.

Hello,

I’m a little confused on AGI and MAGI. I know a Roth is based on MAGI, which I assumed was always your gross income before the standard deduction. In your example the income you use for a Roth conversion is after the standard deduction which gives you an extra 24,000 to convert. Is this right? Thanks for your answer to this question.

Bill

Bill, sorry for the delay in responding, I struggle at times to keep up with the comment flow. I ran the numbers by my CPA, and I had used the $24k standard deduction in my calc. She said I was good to go, so I’m assuming she looked over the details. Something you should check with your own CPA before doing a ROTH conversion. I certainly hope my CPA was correct, guess I’ll find out for sure when she does my taxes in a few months!

I don’t understand the “55 retire rule”. How does the IRS know that you retired exactly at 55?

I’m planning on retiring next year. I’ll be 54 when the year starts. And 54 when I leave my company. BUT, in the tax year I’ll be retiring, I’ll be 55.

I never realized doing a Roth conversion has to take place when you are 55 or older.

Am I confused?

Jack, I can appreciate the confusion, and I’ve no idea how the IRA knows how old you are when you retire. However, my understanding is that you must be age 55 when you retire, not just in the tax year (based on this article, but you should conduct your own research or talk to your HR folks). I don’t think I’d risk it, and I’d assume the IRA WILL know how old you were when you retired. Something you should discuss with an “expert” who knows your personal situation, for sure.

As for waiting until age 55 or older to do a Roth conversion, the primary driver is the fact that before-tax withdrawals are penalized before that age, unless you can use any of the exceptions outlined in this article.

I’ve been looking into the conversions also as I’m worried about our very heavy 401k pre-tax vs Roth balances and the potential RMDs we’d have in a little over 10 years. My financial advisor told us to fully fund Roth 401k a few years ago, but then I learned that the 401K Roth amounts will still be used for RMD calculations so I decided to just keep with the tax break now with the standard 401k contributions.

I was considering using up all my 22% and some of 24% bracket this year with Roth conversions but ran into a limit of being able to take advantage of thr American Opportunity tax credit (for those with college kids, it’s a great one!). That will cause me limitations at about the $180k AGI level, if I still want to get that credit. So folks may want to keep that in mind if they have college kids.

Does anyone have advice on the best way to find a CPA, and maybe one who can help with not only this type of conversion advice but also understands geo-arbitage (how to work the tax system for state taxes if we decide to retire while in a tax free income state but then may be roaming around the country or international for years after that)? Turbotax has always been sufficient for what I’ve needed, but I may be getting to the point of needing advice for this bigger dollar implications. Thanks!

Avoid that by rolling Roth 401K over to Roth IRA prior to age 70 1/2.

Thanks Dave, I was thinking that also. Just another step I’d have to take rolling out of my employer 401K (government TSP) to another institution.

Dang, you’re QUICK, Dave! Exactly the answer I was going to give, but you got to it only 9 minutes after Jeff posed the question. I’ll need to hire you to respond on my behalf, tough to keep up with the comment flow at times. Thanks for jumping in with sound advice, I’m planning on doing exactly that rollover (401K Roth to IRA Roth) to avoid the RMD issue, though part of me wonders if future legislation will also mandate RMD’s on IRA Roth’s….

Jeff – glad to have Dave jumping in on the 401(k) Roth RMD question, and I agree with his advice. As for “how to find a CPA”, you may want to try Palladin, a free referral service that I have on my Resource page.