The most popular post I’ve ever written was titled How To Build A Retirement Paycheck, which outlines the details of how we were setting up The Bucket Strategy for retirement. It seems a lot of you have an interest in the topic, for good reason. Moving from the Accumulation Phase to the Withdrawal Phase is one of the biggest challenges in retirement, and The Bucket Strategy is the method we’ve chosen to manage the transition.

However, that post was missing something that several of you have asked about. The questions revolve around the issue of how to manage the bucket strategy in retirement. Since I’ve now experienced 18 months of living with The Bucket Strategy in retirement, I felt it was an appropriate time to address what we’ve been doing to manage the bucket strategy. This is Part 2 of The Bucket Strategy Series, other posts are listed below:

Today’s post was triggered by a recent email from Neil, who’s question is similar to other inquiries I’ve received on how to manage the bucket strategy in retirement. Neil is one of only a few loyal readers I’m aware of who has read every single post I’ve written, so I’m rewarding him by sharing his well-worded email in its entirety below (thanks, Neil for your agreement to share with all of our readers).

It’s a good summary of the type of questions I get regarding how to manage the bucket strategy, so I trust all of you that have similar questions will benefit from this post.

I’ve bolded a few of the relevant highlights in the email:

The Reader E-Mail That Triggered Today’s Post:

Fritz,

I discovered your blog this year and read it from post 1 to the present. I’ve derived a tremendous amount of value from following your path. So – thank you! I’m a little older than you and deciding when to retire as I’ve reached FI, but still enjoy work and the income it brings. I have to admit that I worry a lot about the sequence of return risk. I don’t want to retire at the top of the market.

Here’s my specific question. Assume for this case study that I have $1M in my retirement fund (am planning for $40,000 in expenses), invested 60/40 (the allocation percentage is not that important for this question). If I was to implement a bucket strategy I would probably have

$600,000 in equities

$320,000 in bonds

$80,000 in cash for two years of expenses.

So year 1 I withdraw $40K to live on, and the market does a 2008 and drops 50%. At the end of the year I have:

$300,000 in equities

$336,000 in bonds (bonds went up 5% in 2008)

$40,000 in cash

Total assets of $676,000, with a need to withdraw $40,000 for expenses.

In that scenario, what do you do? Do you rebalance at year-end ($405K/$231K/$40K)? if you do you’ll supposedly capture the gains on the way back, but you now have less than 7 years in “safe” assets. If the market goes up in 2009, do you rebalance again? Just wondering how you see yourself implementing the bucket strategy in a down/volatile market and if there are any resources that you have used to come up with your strategy?

Regards,

Neil

To Neil’s final question of “are there any resources that you have used to come up with your strategy?”, I had to confess in my response that the answer was “No”. Today, I’m rectifying that situation with this post.

This one’s for you, Neil! (You’ve earned it, I still can’t believe you’ve read every post I’ve ever written!)

How Hard Is It To Manage The Bucket Strategy?

One of the concerns people cite when considering the bucket strategy is “Will it be difficult to manage?”, which is really the question at the core of Neil’s email. After 18 months of managing our bucket strategy, I can testify that it’s been easier than I expected it to be. After establishing the basic structure as outlined in my original post on The Bucket Strategy, I would estimate my annual time commitment to manage the strategy is less than 5 hours.

Today, I’ll walk you through the steps I take as I manage The Bucket Strategy in retirement.

Setting up the bucket strategy is the most important part, but is outside the scope of today’s post. If you’re interested in the steps required to implement your buckets, refer back to the original post. It’s my most popular post for a reason, and there’s no reason to re-state that content here.

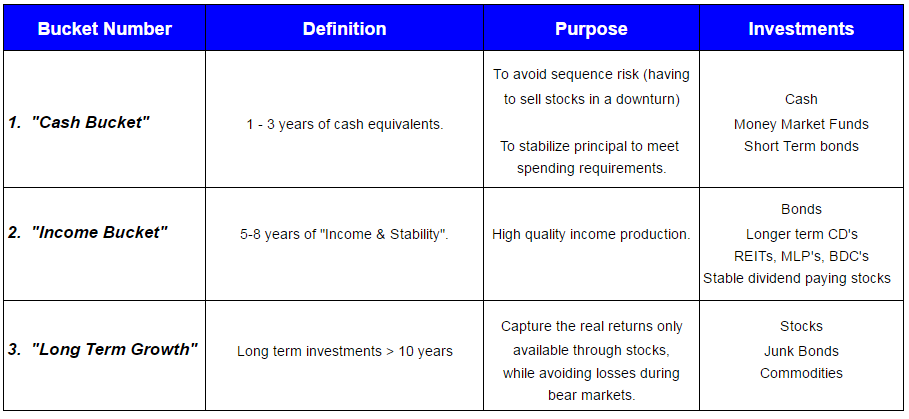

As a refresher, below is a summary outline of the strategy:

Below, I’ll outline the steps I follow now that I’m in retirement, which should answer your questions on “How to manage the bucket strategy in retirement”.

Steps To Manage The Bucket Strategy

To start, it’s worth mentioning that my bucket strategy remains exactly as outlined in the original post. At this point in retirement, I’ve not made any changes to the basic structure. I’m pleased with the effectiveness of the strategy in:

Minimizing my worry about Sequence Of Return Risk.

Creating a discipline to ensure we stay within our Safe Withdrawal Rate.

Creating a methodology to deal with the unexpected expenses we all face (expensive car repair, etc.)

As mentioned in the original post, I still use the CapitalOne360 account as a “sub-bucket 1”, where all of our annual spending is initiated via a monthly transfer to our checking account. Determining the amount of our “monthly paycheck” is Step 1 in the process:

Step 1: Determine Your Monthly Paycheck Amount

As mentioned in A Step-By-Step Guide To Your Annual Financial Update, I update our Net Worth every January. Once I’ve determined the total amount in our “retirement accounts” (Net Worth excluding cars, house, etc.), I calculate the Safe Withdrawal Rates using 3%, 3.5%, and 4% rates. I also review our annual spending from the prior year (see Step 5 below), and determine the annual spending which will be covered via investment withdrawals for the New Year.

For 2020, we’re keeping our “investment spending” consistent with our 2019 level. Given the strong growth of our portfolio in 2019, our SWR will be decreasing slightly in 2020.

Once the annual spending from investments is determined, I adjust our monthly ACH transfers from CapitalOne360 to our checking account, if required. Since no change was required for 2020, I move on to the next step.

Step 2: Refill The “Paycheck Account” for the New Year

To simplify the calculation of spending in a given year (see Step 5), I’ve found it’s easiest to refill the CapitalOne360 account at the beginning of the year and then avoid moving any additional money into the account during the year. I view it as a bit of a “Measuring Cup” approach, where the CapitalOne360 is used as a “protected” subset of Bucket 1. By avoiding moving any additional money into the account during the year, tracking our annual spending is a simple as comparing the beginning vs. the ending value, a step that gets “messy” if you have any unnecessary transactions in the account.

To manage the inevitable “slop” of moving money around, I use our Vanguard Money Market account to capture any asset sales (or unexpected income) during the year. As a general rule, I target 18 months of spending in the CapitalOne account in January, which draws down to 6 months of spending by December. Then, I use the cash in the Vanguard MMF account to refill the CapitalOne account back to the 18 month level after year-end.

Step 3: Refilling Bucket 1

The main purpose of The Bucket Strategy is to avoid selling stocks during a bear market. Since bear markets frequently start with an aggressive downward move, it’s important to us to keep our Bucket 1 as close to “full” as possible throughout the year. By looking at our CapitalOne360 balance at any point in the year, we can see how much of our Bucket 1 funds have been withdrawn (starting balance minus current balance), and how much of a “refill” is required to keep Bucket 1 “full”.

I don’t have a set schedule to refill Bucket 1, but have found I typically execute a “refill trade” 2-3 times per year. The general principle for a refill trade is this:

If stocks are up, sell stocks.

If stocks are down and bonds are up, sell bonds.

If both stocks and bonds are down, continue to draw down Bucket 1 (no refill).

The easiest way I’ve found to analyze what to sell is to log in to our Personal Capital(affiliate link) account and compare our current Asset Allocation vs. our year-end allocation (or, you can compare to your Targeted Asset Allocation using this methodology). If our asset allocation in stocks has moved up, it indicates option 1 is preferred. I then look through our after-tax portfolio of stocks/mutual funds to determine what to sell.

Of interest, all of our “refill trades” have been done via selling equities and REIT’s to date (no surprise, given the strong market since our June 2018 retirement). Since we don’t want to “disturb” our CapitalOne360 balance (see Step 2), I keep any refill money in our Vanguard MMF until the year-end, when I transfer it to CaptialOne as outlined in step 2.

A note about dividends. You could choose to redirect any dividends into your MMF rather than having them automatically reinvested. This could serve as a slow refill of Bucket 1, reducing the amount of refill trades required. We’ve not yet taken this move, but I’ve considered it.

Finally, it’s also important to note that any unplanned income (book sales?) is diverted from our checking account into our MMF fund and used to reduce asset sales required to keep Bucket 1 full.

Step 4: Rebalance Your Portfolio

As Michael Kitces points out in this article, It’s critical that you rebalance your asset allocation in conjunction with the bucket strategy to optimize your returns over time. The following graph from that article highlights the importance of rebalancing your portfolio.

Source: M. Kitces

I rebalance annually as outlined in A Step-By-Step Guide For Your Annual Financial Update. As part of this exercise, I also evaluate the funding level in Buckets 1, 2 and 3 (see the above link for details). Both the asset rebalancing and the macro bucket refill process are conducted once per year, which I’ve found sufficient to keep things on track. I’m also executing Before-Tax 401(k) rollovers to a ROTH every year, which is also a time I look at making adjustments in Buckets 2 and 3, but outside the scope of today’s post.

Step 5: Track Your Annual Spending

To ensure you live within the spending limits dictated by your Safe Withdrawal Rate, it’s critical that you have a method to track your annual spending. As I outlined in this post, we don’t budget. Rather, we simply spend what we have in our checking account and do a year-end calculation to determine our actual spending for the year. Assuming we’ve kept our CapitalOne360 account “clean” from any unnecessary transactions, it’s a 5-minute exercise to determine our spending.

We simply compare our CapitalOne360 beginning vs. ending balance and add any direct deposits we’ve had in our checking account (e.g., pension) which I track in a separate spreadsheet during the year. As simple as that, we know what we’ve spent in the previous year.

Easy…just the way I like it.

My E-Mail Response To Neil

While I had not yet written this post when I responded to Neil’s email, you’ll see consistency with the general response I provide and the detailed overview provided in this post outlining how to manage the bucket strategy.

Below is my response to Neil:

– Essentially, I attempt to always keep Bucket 1 “full” in a decent market. For example, in 2019 I’ve been selling tranches every 3-4 months to match my “paycheck withdrawals”, so my Bucket 1 has remained full in spite of my monthly paycheck. So, your example of having it fall to 1-year balance before a bear market could be mitigated a bit by keeping it topped off as long as the markets are participating.

– Secondly, I’m working to keep my Bucket 1 at 3 years, so I have a bit more dry powder than your example. Something each of us has to determine based on our risk tolerance, but something you may want to consider.

– So….if the market does a 2008, I should have close to 3 years before I’d have to react. In your specific example, I’d likely sell enough bonds (since they were up 5% in ’08) to get back to a 1-2 year cash reserve in Bucket 1. I’d also likely look at reducing the spend a bit given the bear market, so the $40k in your example may actually cover ~15+ months of living expenses.

The basic principle is to allow Bucket 1 to drop a bit in a bear and be patient refilling it until it got to <1 year of expenses. At that point, I’d look at selling anything that was up and avoid touching the equities until they had time to recover. With $336k in bonds in your example, I’d look at using that until the equity portion had rebounded. I’ve also got some other assets (eg., REITs, commodities) which I could selectively sell and am hopeful that something would be up when the equities were down, the basic premise behind having a diversified portfolio.

Good point about having other resources to go along with my (very popular) bucket post. I’ll add it to my list of posts in my queue, I think other readers would also find it of interest.

Fritz

Conclusion: How To Manage The Bucket Strategy

So there you have it, how to manage the bucket strategy in retirement. I’ve been pleasantly surprised at how easy it’s been to manage over the past 18 months but realized it’s been simplified by the strong tail-wind of the generous stock market. Even with that tail-wind, I’m comfortable that we have a plan in place for how we’ll react when the looming bear market attacks.

I’m also sleeping well at night with the benefits provided by The Bucket Strategy:

Minimizing my worry about Sequence Of Return Risk.

Creating a discipline to ensure we stay within our Safe Withdrawal Rate.

Creating a methodology to deal with the unexpected expenses we all face (expensive car repair, etc.)

Simplifying the tracking of our annual spending.

While some, like my friend Big ERN, may argue that returns could be improved by using other strategies, I am confident that the bucket strategy is the right approach for us. The value of that restful sleep is worth a bit of return, in my view.

After all, we all want to sleep well in retirement, right?

Your Turn: Are you using The Bucket Strategy to manage your withdrawal phase in retirement? If so, have I missed anything that should be included in a post about how to manage the bucket strategy? Let’s chat…

65 comments

Fritz – add me to the list of those who have read all of your posts (some many times over!). They have been super helpful – we are two months into this “new chapter” and the many insights from you and your followers have been huge. My plan is to transfer our monthly “budget” each month directly from our Vanguard Money Market account (which holds 1- 3 year funds). Not as “automated” as your scheduled transfers from CapitalOne360 account, but I think it serves the same purpose? Appreciate your perspective. If your ever in West Michigan, let’s go for a mountain bike spin. I have an extra bike! We have nice trails over here.

Kirk, Welcome to the “100% Club”! At this point, you’re one of only 3 members I’m aware of who have read every post. Thanks for your amazing loyalty to The Retirement Manifesto, much appreciated!

As for your question, I do think the VG MMF will work for you, though if you have a lot of other cash flowing in/out of the account it will make your year-end expense analysis a nightmare. If you’re not using The Bucket Strategy to also track your spending, your system will work fine. Thanks for the offer of mountain biking in Western MI, I grew up in Hillsdale and almost went to WMU in Kalamazoo! Small world, hope to experience your local trails sometime.

we’re employing a similar bucket system, fritz, even though we’re still working 1.5 jobs in our house. rebalancing to a target asset allocation i see as a big key. our fixed income is mostly in preferred stock etf’s that pay out a pretty high % compared to gov’t bonds these days. currently we reinvest that significant income but will probably use it more like an annuity when we pull the plug on work. those things pay out monthly which is nice for a sort of “normalcy” as part of a regular paycheck. right now it’s a simple 70/15/15 stocks/fixed/cash allocation and we’ll likely raise the last 2 a couple of % over the next few years.

like you said, we’re also willing to sacrifice some returns in order to sleep well at night with a big ol’ cash cushion. it’s great to read how people are executing a strategy in real time, so thanks.

Freddy, I put a lot of faith in the work of M. Kitces and found his article on the importance of rebalancing when using The Bucket Strategy as a great analysis. Definitely important to incorporating rebalancing into your “maintenance program”.

Fritz, I am not quite retired yet but since I’ve been following your blog I have been setting up our investments into the buckle system to get an idea of how our investments will fit into the three buckets. I see that you are replenishing bucket one by selling securities, but my idea is to stop reinvesting my dividends and capital gains and let that income flow into the money market account that I will then draw from to refill our checking account. Do you have any thoughts as to which method may be better in the long run, taking divs and capital gains in cash vs reinvesting them? My thoughts were that once I reached retirement my investments would kick out enough income plus SS to replace our paychecks without having to reduce our share balances.

As I told you in my last comment we are both 62 and are considering retiring at the end of this year, so I’m really trying to get my head around exactly how to set up my buckets for the most tax efficient withdrawal method.

Again I just want to say I really enjoy your posts and look forward to eventually getting all of them read.

Dale

Dale, using your dividends/cap gains as a “drip refill” is certainly a viable option, and I really do think it’s a “wash” if you let them drip into your Bucket 1 or let them reinvest (then, sell targeted assets to refill). I think we’re splitting hairs at this level, and would have no qualms recommending that you follow the “drip refill” if it’s more comfortable to you. I actually changed my dividends to auto deposit into my MMF, then changed it back after a few months when I decided I’d rather decide what I want to sell for my refill moves.

Congrats on closing in on The Starting Line (hopefully) later this year. I’m pleased to play a small role in your journey.

Dirk Cotton wrote a good and IMO very even-handed article on this subject a few months back, see http://www.theretirementcafe.com/2019/04/a-good-many-retirees-seem-to-be.html

As usual, the comments to the post help flush out some of the points – including your issue of you choosing what to sell and, of course, when to sell it rather than “forced” sells at pre-determined dates.

Great resource. I respect Dirk’s work, it’s a great addition to the discussion. Thanks for taking the time to find it and share the link with everyone. Definitely worth a read. I love his discussion on the “free dividend fallacy”.

Three years into retirement and what has worked for us is 1) dividends not reinvested, not only to refill Bucket 1 but as an unemotional decision put on auto pilot; 2) four debt-free residential rental units that we actively manage, another unemotional source of monthly cash; 3) an enjoyable side gig that brought in $6,000/year; 4) delaying SS in order to capture capital gains over a four year period in order to reduce exposure to more volatile stock sectors and 5) using the last year of work to move quite a bit of cash into bucket 1 in order to complete costly remodeling projects, travel and other retirement dreams no matter what the market has in store – to date, we have not had to do any additional withdrawals. Sleeping well at night is the goal knowing that returns could have been a higher but so would the risk. Good luck with your planning!

Great answer to Neil. And great explanation of how to refill the buckets. Our approach is very similar. We have a year’s worth of expenses in cash and a short-term bond fund worth about five years of expenses. Every month $1,500 is diverted from our short-term bond fund and deposited into our checking account. Add to that our monthly pension of $1,643 and we’re good to go. All we really do now is rebalance once a year. Our retirement is basically on autopilot. And everything’s working, and we can sleep soundly at night. Take that, dreaded sequence of return risk!

Glad to know you’re using a similar approach, Mr. G. It really is as close to autopilot as I could get it, and I’m pleased with the minimal effort required to keep our airplanes on their desired course. Thanks for reinforcing the simplicity of the approach.

Thanks for another great post Fritz. I am in the final stages of perfecting your bucket strategy. I am a little conflicted based on other retirement bloggers guidance. I am trying to stretch my non retirement assets to last before the Feds ask for some of my tax advantaged retirement plans back due to RMDs. Other bloggers contend to used equities in those non retirement assets to avoid any income generated from bonds which would be taxed at a higher rate than qualified dividends and LTCG, in order to convert more traditional IRA monies to Roth while minimizing taxes. However, I would need to be in bonds to comply with step 2 of your bucket strategy since I am 12 years away from mandatory RMDs.

I can relate to being “a little conflicted”. A big part of retirement planning is to review trusted resources and determine for yourself what your approach is going to be. It’s helped me having this blog to share my strategies and logic, and I’m pleased that my words are helping others plan their routes. Even if it makes them a bit conflicted…

I suspect that many of the financial independence bloggers and personalities don’t actually have a withdrawal rate after they hit FI. They either have enough passive income streams from real estate, pensions, etc. or they make enough from their blogs, courses, speaking engagements, etc. to sustain their lifestyles without using any of the dividends and growth from their portfolio’s. Or if they are like me, they get zero from blogging but have some kind of lucrative part time hobby job that pays all, or most, of their cost of living. I think the bucket approach still applies to us, but mostly as an insurance program. For us the bucket is a reserve fund that will only be used if there is some interruption in the flow of outside income. I consult on an annual contract and so I never know if my clients are going to renew for another year. I am carrying enough cash equivalents to support my family until I hit age 70 when I’ll take Social Security even though I haven’t touched the bucket in my first four years of retirement. How do you see the bucket strategy for people who are retired but still have an income that supports 100% of their spending?

Interesting suspicion, Steve. I’ve never seen the numbers, but would agree that most driven folks do tend to have more income in retirement than they thought they would. Whether it’s sufficient to eliminate withdrawals is the question. For those who have a gap, The Bucket Strategy is easily adjusted to accomodate any unplanned income, as I explained in the post. For those, like yourself, who have excess income in retirement, the principle of having a cash reserve is the most important takeaway. In either case, I think the principle element of thinking about your risk exposure in terms of time is the most important application of the strategy.

Just a thought, but might Steve’s concern be that his cash reserve is growing (having started out as “enough cash equivalents to support my family until I hit age 70” as his need for it diminishes – ie time to his commencing SS at age 70 has now reduced by 4 year?

Perhaps, though having “too much cash” due to unplanned income isn’t a bad problem to have! Steve, can you clarify your concern, and let me know if I’ve answered it with these comments? Thanks.

I wasn’t worried about having excess cash, I could move it to bonds since I’ve got all the equity exposure I need but wasn’t in a hurry in a declining interest rate market. Because I liked my job I worked well past FI, plus I inherited extra money so I don’t really worry about maxing growth, in fact my 50% equity portfolio is fine for me. I’m actually keeping even with inflation with money markets right now.

I agree not a problem!

And in due course, I guess, what it may come down to is a personal trade-off of the:

a) opportunity cost of holding a lot of cash (or cash equivalents) in a bull market

versus

b) increased liquidity and security of holding cash in a bear market

Fritz,

Another great post. Thanks. I have embraced the bucket strategy and our portfolio is roughly 60% equities, 35% bonds and 5% cash. My wife and I are 65 and 64 respectively. My former employer offered a lump sum or a pension and I took the pension as combined with our Social Security (my wife and I both had successful careers) are “necessary” expenses are covered. If I hadn’t had a pension I would have seriously considered a SPIA as I see a lot of “peace of mind” in knowing required baseline expenses will always be covered. One additional thing that we have done over the past 25 years of marriage is to record our expenses (anything greater than $5) in a budget book. (I know that many use Quicken, however it is REALLY easy to record expenses by hand). I know this is “old school” but it gives me tremendous insight (and peace of mind) to see expense trends in discretionary expenses. Case in point….I play golf twice a week at various public courses across greater Los Angeles and in the course of a year, my wife spends more money at the hairdresser than I spend playing golf! We both have our “luxuries” and this keeps us in sync. In 25 years we have never had an argument over Money!

Fred, you’re among the lucky few who have their “necessary” retirement expenses covered through a pension and SS. I may be close to that level once we start SS at Age 70, though we’ll have to see what inflation does between now and then (my pension is fixed). Good point about the SPIA, I also thought about purchasing an annuity, but am holding off for now with the high coverage ratio from my pension. I may consider it as a longevity risk hedge, but I’m waiting for interest rates to come up a bit before I get serious about it.

I love your “old school” expense tracking, and congratulate you on your mutual agreement over all things financial. One thing is clear…you have to play more golf (or, throw a trip to Pebble Beach into the mix! 🙂

Regarding your answer, don’t you need to use some of the $336,000 in bonds to rebalance the equities?

Perceptive comment, Dan. Yes, Step 4 would likely trigger a reallocation, though I wrote the more detailed steps after I had initially responded to Neil, so that bit wasn’t included in my response. I’d also likely decide if I was going to sell bonds to refill bucket (or draw bucket 1 down) before I made a decision on the stock/bond reallocation move. While the “rules” appear hard and fast, in reality I will be using some subjective opinion when things get dicey.

Agree with everyone else Fritz great write up. I was wondering if you have some spare time maybe putting all of what you wrote in words into some sort of diagram or flow chart might also be useful for those that are more visually inclined. You could show the $ flow between the buckets and how with buckets 2 and 3 sometimes money can go back and forth between them to rebalance.

“…if you have some spare time…” being the critical disclaimer.

I’d love to do another infographic, but afraid I’m struggling in keeping up with the writing, reader responses, book writing and charity work at this point.. Glad to hear you like the visuals, I’m also a big fan but, unfortunately, they take quite a bit of time to put together. Thanks for the suggestion, hope you still love me even though I have to say no at this time. Wink.

Sounds busy, are you sure you are retired? 🙂 Yeah I think I can handle no infographic, I went back to the original bucket post and was surprised I’ve been following you for 3+yrs!

Great break down Fritz. I kind of follow the strategy myself even though I still work half-time. I keep a nice cash reserve in a high-yielding money market fund and keep replenishing that when and if needed. The good news for me is my side hustle has been taken off so much that it’s supplemented my living expenses well, to the point of covering about a quarter of them. Ideally I’ll get that number up to 100% at some point, but only if I still enjoy doing it.

Thanks for the kind words, Dave. Good luck growing that side hustle income, you’re crushing it!

Thanks for a great article! How do you classify REITs? As part of the stock % of your portfolio or more like a bond?

I have REIT’s in my 10% “Alternatives” allocation, so I have a target of 50% equity/40% cash & bonds / 10% alternatives. Given that they’re “bond-like”, I map them to Bucket 2.

Perfect timing! I am 12 mo away from pulling the trigger and had just started thinking about how our cash bucket would get refilled! Had just re-read your original post a few days ago after going through the ‘1 year to retirement’ checklist. I had assumed in down years you don’t refill the cash but I hadn’t yet researched to make sure I was ok with that assumption. I do have a pretty nice pension coming so had planned to have probably 4 year cash buffer so have some time to ride a downturn out.

Thanks for the post!

I wrote it for you, Cathy. Wink. Good luck as you approach The Starting Line!

I also plan to use some variation of this bucket strategy when we’re FIRE. Some planned tweaks to what Fritz is doing:

1) Stop DRIP in the equities portfolio. Since we will use the dividend cash and in addition, sell assets, I want to be more active in what/when I buy during re-balancing. DRIP is great if you have a constant surplus of cash coming in but taking the dividends and spending it to live is, IMO, the spend version of dollar cost averaging.

2) Per the article, “Given the strong growth of our portfolio in 2019, our SWR will be decreasing slightly in 2020.” I also plan to tweak my equity SWR for the year based on some calculation using the CAPE ratio. But my range will go down to as low as 2.5% when I think the market is “very overvalued” compared with historic CAPE ratios.

Fritz, I’m curious if you use any specific indexes or formulas to determine your 2020 withdrawal rate.

3) Our cash cushion will be closer to 5 years of essential spend. So during more “lean” years, the extravagant travel and non-essential big ticket items will be deferred (e.g. That 10 year old car can last a few more years than originally planned, we’ll defer that overseas month long vacation, etc.)

My idea is to make things comfortable and simple and not optimize every bit of return if it adds more complexity/stress than it’s worth. Hopefully we’ve accumulated enough asset that we can sacrifice some return to buy that reduced complexity/stress.

Phillip, yours looks like a solid plan and I’m sure it’ll work well for you. I am a big fan of CAPE ratio, but don’t use it to formally establish my SWR. I do factor in the market valuations when I’m doing my year-end review, and look at things as highly valued at the moment. This naturally drives down my SWR given my portfolio’s growth in 2019 with my spending level remaining constant. I think the CAPE is a solid approach, and look forward to hearing how it works for you when you get to the stage of implementation. Let’s keep in touch.

I am retired and have a base income so the income bucket is what I call Bucket +. If I have more than a few years of income + but the market is up, I refill my Income + bucket ahead of plan. If I have more than a few years of income in a Money market, so be it. Most significant downturns last 2-3 years. So if the market is up, like this year, as long as taxes aren’t negatively affected or planned Roth conversion aren’t hit I, take some profit ahead of schedule. More is better then less.

Dale, no need to take more risk than is necessary, and I agree with you than any incremental income doesn’t hurt you if it sits in cash (given that it’s more than you expected in your base plan and related asset allocation).

Hi Fritz,

I’ll echo others comments by saying your site content is fantastic and feedback from other readers is INVALUABLE! My question is, how do you mix in taxable, tax-deferred and tax-free investment sources into your bucket/bucket refill strategy ? Also, do you maintain a separate bucket to ‘pay’ for Roth conversions? Perhaps bucket #1A?

thanks

Sandy

I was going to write a similar question as Sandy. I have amp up my Roth conversions with the current reduced tax bracket incentive, which basically has totally changed my bucket allocation dramatically for me. Since I am over 59 1/2 the money is immediately available to withdraw in an emergency. The dividends and interest in the Roth, add quite a bit of cash monthly and I do the reinvestment instead of using Drips. I can’t wait and do a yearly asset allocation rebalance-maximum I can go is every three months. I do estimated taxes, so these payments I take from my SS equivalent Railroad pension . The government giveth monthly and I return a portion quarterly. After 21 years of FIRE, lots of changes have happened and I find myself not adhering to a strict bucket structure. Lara

INVALUABLE!? Wow, even in all caps. I appreciate the kind words!

Good question on how I view the tax status of the buckets. It’s a valid question and one I didn’t specifically address in this post. To the extent possible, I try to keep my Bucket 1 in after-tax to maximize liquidity. I’m doing Before-Tax rollovers to a Roth every year as I explained in a post last month, so I make asset allocation adjustments (if required) for Buckets 2-3 during that time. If I consume all of my after-tax money, my plan is to use Before-Tax money before I tap into the ROTH money, so I tend to have more of the Bucket 2 assets in my Before-Tax 401(k).

As for paying the tax on Roth conversions, I consider this as part of my baseline spending and include it in my Bucket 1 calculations. I pay quarterly estimated taxes, which include my estimated tax on conversions, so it’s a pretty steady flow of tax spending throughout the year. If I were to pay this once per year, I would set up a sub-account in my CapitalOne360 (having the ability to set up sub-accounts is a great feature in CapitalOne) and transfer the money once per year when the taxes were paid. If I did it this way, I would include that estimated amount in my SWR calculation to ensure I didn’t overspend. Hope that helps.

Thanks, Fritz for giving more details. I too think holding off tapping Roth money makes the most financial sense. Lara

Thanks Fritz, yes it was helpful. Reading (and re-reading) your Roth conversion post 🙂

Good post Fritz. Like a reader above, my plan was to build up my High Yield savings account (my paycheck account) in my last year of work – but the last year was cut short before I reached my goal. With 8 more months to go before 59 1/2, I am working to avoid the need for selling out of the brokerage account. So far, the expiration of CDs has allowed us to continue without selling other than some MM funds. Second car has been sold. Cash flow was further improved when we decided to sell the house – I no longer need to replenish my self directed housing escrow account since this years taxes are paid and insurance won’t renew until July. As long as we sell before July, that is.:) And since we are moving cross country with some extended storage, the wine cellar needs to be emptied – so we are saving a fortune there. Roth conversions will start once I am in a lower income tax state.

I’ve been more complex than I probably needed during accumulation. But it was part of the hobby. Now I am trying to simplify. I fear that what I have assembled is too complex for my wife to sustain, if it becomes necessary. So simplifying will make it possible for her to manage it and avoid getting suckered by a “broker” in the future.

Kev, thanks for providing insight from the perspective of someone who was “cut short” on their retirement timing. I’ve done some research, and ~60% of folks end up retiring sooner than planned, so your insight is of great value. I agree with you on the goal of simplifying things in retirement. As I’ve selected things to sell, part of my goal has been to simplify. I’ve also told my wife to use Vanguard’s Personal Advisory service if I exit early. Always good to keep the spouse in mind when managing these things. Good comments, thanks for stopping by.

One thought on dividend paying stocks. My dividend payers represent a bit over 25% of my SWR. I had switched most to pay into the MM account (within the brokerage account) but I’ve since revised that to be more selective. Stocks that are down I reinvest dividends. Those that are flying I take the payout. It allows me to buy low selectively, which should juice the returns a bit.

For a short period I was pursuing very high dividend payers and preferreds – but I exited most of those. I might do a fund of them, but just got sleepless chasing yields in individual securities. Too many things I have neither time nor knowledge to track. I have to resist my tendency to follow shiny objects.

Instead of carrying so much cash for essentially the full span of retirement, what would be your opinion of leaving a significant portion of Bucket 1 invested and having credit on standby to use in the event of a market downturn? I have seen the suggestion to use a reverse mortgage instead of selling stocks during a downturn. In our case we have a low rate (5.5%), interest-only Home Equity Line Of Credit with zero balance, left over from some remodeling. Instead of selling stocks, we could tap the HELOC, pay only the interest during the downturn and then pay off the HELOC after the market recovers. Over a 30 year retirement and several downturns, would we come out ahead by keeping only a year or so of cash in Bucket 1, leaving the rest invested and only paying the HELOC interest during a downturn? We could replenish Bucket 1 every 4-6 months to avoid drawing that Bucket down uncomfortably low.

Chuck, excellent question and certainly a viable option. I believe I’ve seen M. Kitces propose this (it may have been Wade Pfau?), and it’s an interesting concept. Personally, I just like the convenience of having readily available cash, but I’d have no argument with the HELOC option being a viable alternative.

I found Wade Pfau’s article. A reverse mortgage line of credit looks like it would be a really sweet deal as a standby source of cash instead of selling stocks in a down market or holding a large amount of cash.

Dug a little deeper. Looks like a reverse mortgage HELOC, with its high up-front costs, is best viewed as insurance against running out of money at the end of retirement, and only if you plan to stay in the same house. A conventional HELOC seems better as a standby source of cash to ride through a market downturn and avoid selling stocks.

How does tax planning mesh with the bucket approach? In my case, I either have to take a taxable withdrawal from my IRA/401K or sell securities in taxable accounts to generate cash for monthly living needs. I am only 62, so SS and RMDs won’t kick in for a few more years. Unfortunately, most of my “cash” is in the pre-tax accounts, which I am reluctant to draw on due to the tax impact. I really think that I need to build cash reserves outside of the pre-tax accounts so that I am not forced to take cash out of one of them late in the year which could impact my tax bracket due to capital gains taken earlier in the year, but haven’t thought through the strategy as to how to do that yet. Ideally, I would have cash/investments in taxable accounts to live off of now and then look to pre-tax accounts once RMDs kick in. Thoughts?

Mike, I keep all of my bucket 1 cash in taxable accounts, which I built up on my final year of work (I redirected all of my 401(k) savings excluding the 6% which gets matched into after-tax cash savings. We also downsized our home and banked a lot of the equity into bucket 1).

You may be interested in my post about executing a pre-tax rollover via the “topping off” strategy, which I’m doing every year in spite of being 15 years away from RMD’s. You could follow the same logic, but instead of rolling it over into a ROTH you could move it to after-tax savings for use in Bucket 1. Just a thought. Hope it’s helpful.

I am using the “topping off” strategy to fund my ROTH and take capital gains at 0% federal tax. I do plan on having money to leave to my kids, that is why I really want to fund up a ROTH prior RMDs and SS kicking in. I may need to skip a year or two of taking capital gains and roll money out of my pre-tax accounts into my taxable account and fill up to the top of the 22% bracket (that is where I will be anyway when RMDs and SS both are in play). I really wanted to roll those funds into a ROTH IRA, but probably need to build up some reserves in a taxable account to carry me through the next market down-turn.

Fritz, how do u handle one off expenses? Like replacing the roof, new refrigerator, repairs on cars… these expenses would increase ur withdrawal rate. But u can’t predict how w much.

Great question, and one I addressed in detail in my article: “Our Retirement Investment Drawdown Strategy” (scroll to “Setting Up Our Paycheck / One Off Expense Reserve”). In summary, I set up an annual reserve based on expected life of long-term expenses (e.g., car replacement, house maintenance), it’s explained in detail at that link.

Hey, Fritz. Your response to the “one off” expense question referring back to the 6/20/17 drawdown strategy post that includes a cabin photo, reminded me we have a N GA realtor in common! Appreciate your take on buckets, but wondered if you had any thoughts about the time horizons that are perhaps inferred, but omitted from your chart: years 3-5 and 8-10. These time horizons seem to be of particular importance as several data analyses I’ve read focus on 6 years as being a critical time horizon for equity risk. Additionally, any thoughts on the use of various risk rating provider’s risk potential classification categories (e.g. Morningstar risk 1*-5*, Lipper “preservation of capital” 1-5, or VANG risk potential 1-5) as a tool to align with time horizon and thereby define buckets?

Hmmmm….me wonders which realtor we both know? I know several in the area…

As for mid-long term investments, the longer the horizon the more I focus on stock, so pretty much anything >8 years is an equity investment. For the mid-term (3-7), I focus primarily on bonds. As I’ve mentioned in previous posts, I could theoretically “survive” a 7-8 year span without selling any equities. Finally, I’ve not used any 3rd party risk classifications, but it’s certainly a viable consideration as you’re looking at what allocation to include in each bucket. Hope that helps, thanks for stopping by!

Would appreciate your review of Michael McClung’s “Living Off Your Money”. He has a similar approach with some specific guidelines.

Very detailed analysis.

thanks

Bob

Thanks for the tip, Bob. I’ll look it up. Unfortunately, I have too many books in my “to read” pile already, but I’ll get to it in time! Sounds like it’s worth a read, thanks for sharing.

Hello Fritz,

My name is Javier from Spain, and this is the first time I write to you.

I am close to retirement and have discovered a brave new world in your blog and all these retirement methods to make our money last.

Thank you for this labor of love in your blog. I’m really learning a lot.

Now the question I can’t answer myself on the bucket strategy.

Unlesss I am missing some basic concept (which wouldn’t be unlikely) I conclude that either I use the bucket strategy OR I rebalance my portfolio. I can’t have both.

I mean, either Option 1 I choose an asset allocation (static or dynamic) and stick with it (i,.e. I rebalance periodically my assets), or Option 2 I hand-pick every year which assets to sell from my portfolio (i.e. the ones with positive returns), hence de-balancing my asset allocation.

I don’t see how hand picking which assets to sell to refill my buckets AND then rebalancing my portfolio makes any sense, since when rebalancing I will need to sell what I did’t want to sell in the first place.

Right? (I guess not, but I’d like to hear why)

If the above was right, the I would have to choose between both options.

For option 1 (asset allocation and selling asset classes proportionally to maintain it) I’ve read studies on safe withdrawal rates.. 3-4% rules.

For option 2 I have not seen similar simulations on the bucket strategy, so I wouldn’t know how to compare hard data between the two-

Conceptually, option 2 advocates that it is possible to sell this year what will go down next year and not sell what will go up: Since I don’t know the future, I instead sell what already gave me some benefit in the past and keep what did not, in the hope of cyclical market behaviour. It also (maybe that’s the key) gives me peace of mind knowing that I made a benefit in the sale. Now, that’s not the same as knowing that I sold what will give me less benefit next year.

So the refill decisions for our buckets, basically equals to timing the market.

What am I missing?

Did I get it all wrong?

Javier, thanks for question, and for being a reader of my work, I’m pleased to hear you’re “learning a lot”. As for your question, I don’t view the bucket strategy as being mutually exclusive with rebalancing. In fact, if you click on the Kitces article under bullet 4, it’s critical that you DO rebalance in conjunction with your bucket strategy. In essence, since we sell what is “up” to refill our buckets, it automatically reduces the % of the asset class which has increased the most in the prior year. Since it out-performed, it’s asset allocation should be higher than your actual target, so selling to refill the bucket aligns with the rebalancing trade. Think about it some more, you seem like a smart guy so I think you’ll figure it out. Do an example with $100k, or 10% of your portfolio, which increases to $110k, or 11%. You sell $10k to refill bucket 1, and your asset allocation goes back down to 10%. There’s always a bit of art with the science, but the general strategy allows you to accomplish both.

I have been utilizing the bucket strategy since retiring 3 years ago. I just spoke to a friend of mine that has recently retired ( year ago) and discussed how calm we are compared to 2009. I still owned a business at that time and like everyone else was leveraged. There are benefits to be elderly (64) as outlined on the news. We have seen this movie before and we will get through the recent declines. Being debt free and having 3 years of expenses in cash definitely gives you peace of mind. There are always people that support having a mortgage with the rates so low. I would recommend having as little debt as possible. There are also a significant amount of professed financial individuals that will be and are recommending fixed annuities as the answer to all. I was a CFP at one time and want everyone to realize there is no free lunch. The commissions can and do top 5%.

In closing; keep up the good work.

“Being debt free and having 3 years of expenses in cash definitely gives you peace of mind.”

Michael, thanks for reinforcing the power of having a strategic bucket system in place. Markets like we’re facing today are exactly why they make sense. And, I agree with you on the warnings about fixed annuities, especially given today’s low interest rate environment. Thanks for stopping by!

Fritz – add me to the list of those who have read all of your posts (some many times over!). They have been super helpful – we are two months into this “new chapter” and the many insights from you and your followers have been huge. My plan is to transfer our monthly “budget” each month directly from our Vanguard Money Market account (which holds 1- 3 year funds). Not as “automated” as your scheduled transfers from CapitalOne360 account, but I think it serves the same purpose? Appreciate your perspective. If your ever in West Michigan, let’s go for a mountain bike spin. I have an extra bike! We have nice trails over here.

Kirk, Welcome to the “100% Club”! At this point, you’re one of only 3 members I’m aware of who have read every post. Thanks for your amazing loyalty to The Retirement Manifesto, much appreciated!

As for your question, I do think the VG MMF will work for you, though if you have a lot of other cash flowing in/out of the account it will make your year-end expense analysis a nightmare. If you’re not using The Bucket Strategy to also track your spending, your system will work fine. Thanks for the offer of mountain biking in Western MI, I grew up in Hillsdale and almost went to WMU in Kalamazoo! Small world, hope to experience your local trails sometime.

we’re employing a similar bucket system, fritz, even though we’re still working 1.5 jobs in our house. rebalancing to a target asset allocation i see as a big key. our fixed income is mostly in preferred stock etf’s that pay out a pretty high % compared to gov’t bonds these days. currently we reinvest that significant income but will probably use it more like an annuity when we pull the plug on work. those things pay out monthly which is nice for a sort of “normalcy” as part of a regular paycheck. right now it’s a simple 70/15/15 stocks/fixed/cash allocation and we’ll likely raise the last 2 a couple of % over the next few years.

like you said, we’re also willing to sacrifice some returns in order to sleep well at night with a big ol’ cash cushion. it’s great to read how people are executing a strategy in real time, so thanks.

Freddy, I put a lot of faith in the work of M. Kitces and found his article on the importance of rebalancing when using The Bucket Strategy as a great analysis. Definitely important to incorporating rebalancing into your “maintenance program”.

Fritz, I am not quite retired yet but since I’ve been following your blog I have been setting up our investments into the buckle system to get an idea of how our investments will fit into the three buckets. I see that you are replenishing bucket one by selling securities, but my idea is to stop reinvesting my dividends and capital gains and let that income flow into the money market account that I will then draw from to refill our checking account. Do you have any thoughts as to which method may be better in the long run, taking divs and capital gains in cash vs reinvesting them? My thoughts were that once I reached retirement my investments would kick out enough income plus SS to replace our paychecks without having to reduce our share balances.

As I told you in my last comment we are both 62 and are considering retiring at the end of this year, so I’m really trying to get my head around exactly how to set up my buckets for the most tax efficient withdrawal method.

Again I just want to say I really enjoy your posts and look forward to eventually getting all of them read.

Dale

Dale, using your dividends/cap gains as a “drip refill” is certainly a viable option, and I really do think it’s a “wash” if you let them drip into your Bucket 1 or let them reinvest (then, sell targeted assets to refill). I think we’re splitting hairs at this level, and would have no qualms recommending that you follow the “drip refill” if it’s more comfortable to you. I actually changed my dividends to auto deposit into my MMF, then changed it back after a few months when I decided I’d rather decide what I want to sell for my refill moves.

Congrats on closing in on The Starting Line (hopefully) later this year. I’m pleased to play a small role in your journey.

Dirk Cotton wrote a good and IMO very even-handed article on this subject a few months back, see http://www.theretirementcafe.com/2019/04/a-good-many-retirees-seem-to-be.html

As usual, the comments to the post help flush out some of the points – including your issue of you choosing what to sell and, of course, when to sell it rather than “forced” sells at pre-determined dates.

Great resource. I respect Dirk’s work, it’s a great addition to the discussion. Thanks for taking the time to find it and share the link with everyone. Definitely worth a read. I love his discussion on the “free dividend fallacy”.

Three years into retirement and what has worked for us is 1) dividends not reinvested, not only to refill Bucket 1 but as an unemotional decision put on auto pilot; 2) four debt-free residential rental units that we actively manage, another unemotional source of monthly cash; 3) an enjoyable side gig that brought in $6,000/year; 4) delaying SS in order to capture capital gains over a four year period in order to reduce exposure to more volatile stock sectors and 5) using the last year of work to move quite a bit of cash into bucket 1 in order to complete costly remodeling projects, travel and other retirement dreams no matter what the market has in store – to date, we have not had to do any additional withdrawals. Sleeping well at night is the goal knowing that returns could have been a higher but so would the risk. Good luck with your planning!

Great answer to Neil. And great explanation of how to refill the buckets. Our approach is very similar. We have a year’s worth of expenses in cash and a short-term bond fund worth about five years of expenses. Every month $1,500 is diverted from our short-term bond fund and deposited into our checking account. Add to that our monthly pension of $1,643 and we’re good to go. All we really do now is rebalance once a year. Our retirement is basically on autopilot. And everything’s working, and we can sleep soundly at night. Take that, dreaded sequence of return risk!

Glad to know you’re using a similar approach, Mr. G. It really is as close to autopilot as I could get it, and I’m pleased with the minimal effort required to keep our airplanes on their desired course. Thanks for reinforcing the simplicity of the approach.

Thanks for another great post Fritz. I am in the final stages of perfecting your bucket strategy. I am a little conflicted based on other retirement bloggers guidance. I am trying to stretch my non retirement assets to last before the Feds ask for some of my tax advantaged retirement plans back due to RMDs. Other bloggers contend to used equities in those non retirement assets to avoid any income generated from bonds which would be taxed at a higher rate than qualified dividends and LTCG, in order to convert more traditional IRA monies to Roth while minimizing taxes. However, I would need to be in bonds to comply with step 2 of your bucket strategy since I am 12 years away from mandatory RMDs.

I can relate to being “a little conflicted”. A big part of retirement planning is to review trusted resources and determine for yourself what your approach is going to be. It’s helped me having this blog to share my strategies and logic, and I’m pleased that my words are helping others plan their routes. Even if it makes them a bit conflicted…

I suspect that many of the financial independence bloggers and personalities don’t actually have a withdrawal rate after they hit FI. They either have enough passive income streams from real estate, pensions, etc. or they make enough from their blogs, courses, speaking engagements, etc. to sustain their lifestyles without using any of the dividends and growth from their portfolio’s. Or if they are like me, they get zero from blogging but have some kind of lucrative part time hobby job that pays all, or most, of their cost of living. I think the bucket approach still applies to us, but mostly as an insurance program. For us the bucket is a reserve fund that will only be used if there is some interruption in the flow of outside income. I consult on an annual contract and so I never know if my clients are going to renew for another year. I am carrying enough cash equivalents to support my family until I hit age 70 when I’ll take Social Security even though I haven’t touched the bucket in my first four years of retirement. How do you see the bucket strategy for people who are retired but still have an income that supports 100% of their spending?

Interesting suspicion, Steve. I’ve never seen the numbers, but would agree that most driven folks do tend to have more income in retirement than they thought they would. Whether it’s sufficient to eliminate withdrawals is the question. For those who have a gap, The Bucket Strategy is easily adjusted to accomodate any unplanned income, as I explained in the post. For those, like yourself, who have excess income in retirement, the principle of having a cash reserve is the most important takeaway. In either case, I think the principle element of thinking about your risk exposure in terms of time is the most important application of the strategy.

Just a thought, but might Steve’s concern be that his cash reserve is growing (having started out as “enough cash equivalents to support my family until I hit age 70” as his need for it diminishes – ie time to his commencing SS at age 70 has now reduced by 4 year?

Perhaps, though having “too much cash” due to unplanned income isn’t a bad problem to have! Steve, can you clarify your concern, and let me know if I’ve answered it with these comments? Thanks.

I wasn’t worried about having excess cash, I could move it to bonds since I’ve got all the equity exposure I need but wasn’t in a hurry in a declining interest rate market. Because I liked my job I worked well past FI, plus I inherited extra money so I don’t really worry about maxing growth, in fact my 50% equity portfolio is fine for me. I’m actually keeping even with inflation with money markets right now.

I agree not a problem!

And in due course, I guess, what it may come down to is a personal trade-off of the:

a) opportunity cost of holding a lot of cash (or cash equivalents) in a bull market

versus

b) increased liquidity and security of holding cash in a bear market

Fritz,

Another great post. Thanks. I have embraced the bucket strategy and our portfolio is roughly 60% equities, 35% bonds and 5% cash. My wife and I are 65 and 64 respectively. My former employer offered a lump sum or a pension and I took the pension as combined with our Social Security (my wife and I both had successful careers) are “necessary” expenses are covered. If I hadn’t had a pension I would have seriously considered a SPIA as I see a lot of “peace of mind” in knowing required baseline expenses will always be covered. One additional thing that we have done over the past 25 years of marriage is to record our expenses (anything greater than $5) in a budget book. (I know that many use Quicken, however it is REALLY easy to record expenses by hand). I know this is “old school” but it gives me tremendous insight (and peace of mind) to see expense trends in discretionary expenses. Case in point….I play golf twice a week at various public courses across greater Los Angeles and in the course of a year, my wife spends more money at the hairdresser than I spend playing golf! We both have our “luxuries” and this keeps us in sync. In 25 years we have never had an argument over Money!

Fred, you’re among the lucky few who have their “necessary” retirement expenses covered through a pension and SS. I may be close to that level once we start SS at Age 70, though we’ll have to see what inflation does between now and then (my pension is fixed). Good point about the SPIA, I also thought about purchasing an annuity, but am holding off for now with the high coverage ratio from my pension. I may consider it as a longevity risk hedge, but I’m waiting for interest rates to come up a bit before I get serious about it.

I love your “old school” expense tracking, and congratulate you on your mutual agreement over all things financial. One thing is clear…you have to play more golf (or, throw a trip to Pebble Beach into the mix! 🙂

Regarding your answer, don’t you need to use some of the $336,000 in bonds to rebalance the equities?

Perceptive comment, Dan. Yes, Step 4 would likely trigger a reallocation, though I wrote the more detailed steps after I had initially responded to Neil, so that bit wasn’t included in my response. I’d also likely decide if I was going to sell bonds to refill bucket (or draw bucket 1 down) before I made a decision on the stock/bond reallocation move. While the “rules” appear hard and fast, in reality I will be using some subjective opinion when things get dicey.

Agree with everyone else Fritz great write up. I was wondering if you have some spare time maybe putting all of what you wrote in words into some sort of diagram or flow chart might also be useful for those that are more visually inclined. You could show the $ flow between the buckets and how with buckets 2 and 3 sometimes money can go back and forth between them to rebalance.

“…if you have some spare time…” being the critical disclaimer.

I’d love to do another infographic, but afraid I’m struggling in keeping up with the writing, reader responses, book writing and charity work at this point.. Glad to hear you like the visuals, I’m also a big fan but, unfortunately, they take quite a bit of time to put together. Thanks for the suggestion, hope you still love me even though I have to say no at this time. Wink.

Sounds busy, are you sure you are retired? 🙂 Yeah I think I can handle no infographic, I went back to the original bucket post and was surprised I’ve been following you for 3+yrs!

Great break down Fritz. I kind of follow the strategy myself even though I still work half-time. I keep a nice cash reserve in a high-yielding money market fund and keep replenishing that when and if needed. The good news for me is my side hustle has been taken off so much that it’s supplemented my living expenses well, to the point of covering about a quarter of them. Ideally I’ll get that number up to 100% at some point, but only if I still enjoy doing it.

Thanks for the kind words, Dave. Good luck growing that side hustle income, you’re crushing it!

Thanks for a great article! How do you classify REITs? As part of the stock % of your portfolio or more like a bond?

I have REIT’s in my 10% “Alternatives” allocation, so I have a target of 50% equity/40% cash & bonds / 10% alternatives. Given that they’re “bond-like”, I map them to Bucket 2.

Perfect timing! I am 12 mo away from pulling the trigger and had just started thinking about how our cash bucket would get refilled! Had just re-read your original post a few days ago after going through the ‘1 year to retirement’ checklist. I had assumed in down years you don’t refill the cash but I hadn’t yet researched to make sure I was ok with that assumption. I do have a pretty nice pension coming so had planned to have probably 4 year cash buffer so have some time to ride a downturn out.

Thanks for the post!

I wrote it for you, Cathy. Wink. Good luck as you approach The Starting Line!

I also plan to use some variation of this bucket strategy when we’re FIRE. Some planned tweaks to what Fritz is doing:

1) Stop DRIP in the equities portfolio. Since we will use the dividend cash and in addition, sell assets, I want to be more active in what/when I buy during re-balancing. DRIP is great if you have a constant surplus of cash coming in but taking the dividends and spending it to live is, IMO, the spend version of dollar cost averaging.

2) Per the article, “Given the strong growth of our portfolio in 2019, our SWR will be decreasing slightly in 2020.” I also plan to tweak my equity SWR for the year based on some calculation using the CAPE ratio. But my range will go down to as low as 2.5% when I think the market is “very overvalued” compared with historic CAPE ratios.

Fritz, I’m curious if you use any specific indexes or formulas to determine your 2020 withdrawal rate.

3) Our cash cushion will be closer to 5 years of essential spend. So during more “lean” years, the extravagant travel and non-essential big ticket items will be deferred (e.g. That 10 year old car can last a few more years than originally planned, we’ll defer that overseas month long vacation, etc.)

My idea is to make things comfortable and simple and not optimize every bit of return if it adds more complexity/stress than it’s worth. Hopefully we’ve accumulated enough asset that we can sacrifice some return to buy that reduced complexity/stress.

Phillip, yours looks like a solid plan and I’m sure it’ll work well for you. I am a big fan of CAPE ratio, but don’t use it to formally establish my SWR. I do factor in the market valuations when I’m doing my year-end review, and look at things as highly valued at the moment. This naturally drives down my SWR given my portfolio’s growth in 2019 with my spending level remaining constant. I think the CAPE is a solid approach, and look forward to hearing how it works for you when you get to the stage of implementation. Let’s keep in touch.

I am retired and have a base income so the income bucket is what I call Bucket +. If I have more than a few years of income + but the market is up, I refill my Income + bucket ahead of plan. If I have more than a few years of income in a Money market, so be it. Most significant downturns last 2-3 years. So if the market is up, like this year, as long as taxes aren’t negatively affected or planned Roth conversion aren’t hit I, take some profit ahead of schedule. More is better then less.

Dale, no need to take more risk than is necessary, and I agree with you than any incremental income doesn’t hurt you if it sits in cash (given that it’s more than you expected in your base plan and related asset allocation).

Hi Fritz,

I’ll echo others comments by saying your site content is fantastic and feedback from other readers is INVALUABLE! My question is, how do you mix in taxable, tax-deferred and tax-free investment sources into your bucket/bucket refill strategy ? Also, do you maintain a separate bucket to ‘pay’ for Roth conversions? Perhaps bucket #1A?

thanks

Sandy

I was going to write a similar question as Sandy. I have amp up my Roth conversions with the current reduced tax bracket incentive, which basically has totally changed my bucket allocation dramatically for me. Since I am over 59 1/2 the money is immediately available to withdraw in an emergency. The dividends and interest in the Roth, add quite a bit of cash monthly and I do the reinvestment instead of using Drips. I can’t wait and do a yearly asset allocation rebalance-maximum I can go is every three months. I do estimated taxes, so these payments I take from my SS equivalent Railroad pension . The government giveth monthly and I return a portion quarterly. After 21 years of FIRE, lots of changes have happened and I find myself not adhering to a strict bucket structure. Lara

INVALUABLE!? Wow, even in all caps. I appreciate the kind words!

Good question on how I view the tax status of the buckets. It’s a valid question and one I didn’t specifically address in this post. To the extent possible, I try to keep my Bucket 1 in after-tax to maximize liquidity. I’m doing Before-Tax rollovers to a Roth every year as I explained in a post last month, so I make asset allocation adjustments (if required) for Buckets 2-3 during that time. If I consume all of my after-tax money, my plan is to use Before-Tax money before I tap into the ROTH money, so I tend to have more of the Bucket 2 assets in my Before-Tax 401(k).

As for paying the tax on Roth conversions, I consider this as part of my baseline spending and include it in my Bucket 1 calculations. I pay quarterly estimated taxes, which include my estimated tax on conversions, so it’s a pretty steady flow of tax spending throughout the year. If I were to pay this once per year, I would set up a sub-account in my CapitalOne360 (having the ability to set up sub-accounts is a great feature in CapitalOne) and transfer the money once per year when the taxes were paid. If I did it this way, I would include that estimated amount in my SWR calculation to ensure I didn’t overspend. Hope that helps.

Thanks, Fritz for giving more details. I too think holding off tapping Roth money makes the most financial sense. Lara

Thanks Fritz, yes it was helpful. Reading (and re-reading) your Roth conversion post 🙂

Good post Fritz. Like a reader above, my plan was to build up my High Yield savings account (my paycheck account) in my last year of work – but the last year was cut short before I reached my goal. With 8 more months to go before 59 1/2, I am working to avoid the need for selling out of the brokerage account. So far, the expiration of CDs has allowed us to continue without selling other than some MM funds. Second car has been sold. Cash flow was further improved when we decided to sell the house – I no longer need to replenish my self directed housing escrow account since this years taxes are paid and insurance won’t renew until July. As long as we sell before July, that is.:) And since we are moving cross country with some extended storage, the wine cellar needs to be emptied – so we are saving a fortune there. Roth conversions will start once I am in a lower income tax state.

I’ve been more complex than I probably needed during accumulation. But it was part of the hobby. Now I am trying to simplify. I fear that what I have assembled is too complex for my wife to sustain, if it becomes necessary. So simplifying will make it possible for her to manage it and avoid getting suckered by a “broker” in the future.

Kev, thanks for providing insight from the perspective of someone who was “cut short” on their retirement timing. I’ve done some research, and ~60% of folks end up retiring sooner than planned, so your insight is of great value. I agree with you on the goal of simplifying things in retirement. As I’ve selected things to sell, part of my goal has been to simplify. I’ve also told my wife to use Vanguard’s Personal Advisory service if I exit early. Always good to keep the spouse in mind when managing these things. Good comments, thanks for stopping by.

One thought on dividend paying stocks. My dividend payers represent a bit over 25% of my SWR. I had switched most to pay into the MM account (within the brokerage account) but I’ve since revised that to be more selective. Stocks that are down I reinvest dividends. Those that are flying I take the payout. It allows me to buy low selectively, which should juice the returns a bit.

For a short period I was pursuing very high dividend payers and preferreds – but I exited most of those. I might do a fund of them, but just got sleepless chasing yields in individual securities. Too many things I have neither time nor knowledge to track. I have to resist my tendency to follow shiny objects.

Instead of carrying so much cash for essentially the full span of retirement, what would be your opinion of leaving a significant portion of Bucket 1 invested and having credit on standby to use in the event of a market downturn? I have seen the suggestion to use a reverse mortgage instead of selling stocks during a downturn. In our case we have a low rate (5.5%), interest-only Home Equity Line Of Credit with zero balance, left over from some remodeling. Instead of selling stocks, we could tap the HELOC, pay only the interest during the downturn and then pay off the HELOC after the market recovers. Over a 30 year retirement and several downturns, would we come out ahead by keeping only a year or so of cash in Bucket 1, leaving the rest invested and only paying the HELOC interest during a downturn? We could replenish Bucket 1 every 4-6 months to avoid drawing that Bucket down uncomfortably low.

Chuck, excellent question and certainly a viable option. I believe I’ve seen M. Kitces propose this (it may have been Wade Pfau?), and it’s an interesting concept. Personally, I just like the convenience of having readily available cash, but I’d have no argument with the HELOC option being a viable alternative.

I found Wade Pfau’s article. A reverse mortgage line of credit looks like it would be a really sweet deal as a standby source of cash instead of selling stocks in a down market or holding a large amount of cash.

https://retirementresearcher.com/how-does-the-line-of-credit-for-a-reverse-mortgage-work/

Dug a little deeper. Looks like a reverse mortgage HELOC, with its high up-front costs, is best viewed as insurance against running out of money at the end of retirement, and only if you plan to stay in the same house. A conventional HELOC seems better as a standby source of cash to ride through a market downturn and avoid selling stocks.

How does tax planning mesh with the bucket approach? In my case, I either have to take a taxable withdrawal from my IRA/401K or sell securities in taxable accounts to generate cash for monthly living needs. I am only 62, so SS and RMDs won’t kick in for a few more years. Unfortunately, most of my “cash” is in the pre-tax accounts, which I am reluctant to draw on due to the tax impact. I really think that I need to build cash reserves outside of the pre-tax accounts so that I am not forced to take cash out of one of them late in the year which could impact my tax bracket due to capital gains taken earlier in the year, but haven’t thought through the strategy as to how to do that yet. Ideally, I would have cash/investments in taxable accounts to live off of now and then look to pre-tax accounts once RMDs kick in. Thoughts?

Mike, I keep all of my bucket 1 cash in taxable accounts, which I built up on my final year of work (I redirected all of my 401(k) savings excluding the 6% which gets matched into after-tax cash savings. We also downsized our home and banked a lot of the equity into bucket 1).

You may be interested in my post about executing a pre-tax rollover via the “topping off” strategy, which I’m doing every year in spite of being 15 years away from RMD’s. You could follow the same logic, but instead of rolling it over into a ROTH you could move it to after-tax savings for use in Bucket 1. Just a thought. Hope it’s helpful.

I am using the “topping off” strategy to fund my ROTH and take capital gains at 0% federal tax. I do plan on having money to leave to my kids, that is why I really want to fund up a ROTH prior RMDs and SS kicking in. I may need to skip a year or two of taking capital gains and roll money out of my pre-tax accounts into my taxable account and fill up to the top of the 22% bracket (that is where I will be anyway when RMDs and SS both are in play). I really wanted to roll those funds into a ROTH IRA, but probably need to build up some reserves in a taxable account to carry me through the next market down-turn.

Fritz, how do u handle one off expenses? Like replacing the roof, new refrigerator, repairs on cars… these expenses would increase ur withdrawal rate. But u can’t predict how w much.

Great question, and one I addressed in detail in my article: “Our Retirement Investment Drawdown Strategy” (scroll to “Setting Up Our Paycheck / One Off Expense Reserve”). In summary, I set up an annual reserve based on expected life of long-term expenses (e.g., car replacement, house maintenance), it’s explained in detail at that link.

Hey, Fritz. Your response to the “one off” expense question referring back to the 6/20/17 drawdown strategy post that includes a cabin photo, reminded me we have a N GA realtor in common! Appreciate your take on buckets, but wondered if you had any thoughts about the time horizons that are perhaps inferred, but omitted from your chart: years 3-5 and 8-10. These time horizons seem to be of particular importance as several data analyses I’ve read focus on 6 years as being a critical time horizon for equity risk. Additionally, any thoughts on the use of various risk rating provider’s risk potential classification categories (e.g. Morningstar risk 1*-5*, Lipper “preservation of capital” 1-5, or VANG risk potential 1-5) as a tool to align with time horizon and thereby define buckets?

Hmmmm….me wonders which realtor we both know? I know several in the area…

As for mid-long term investments, the longer the horizon the more I focus on stock, so pretty much anything >8 years is an equity investment. For the mid-term (3-7), I focus primarily on bonds. As I’ve mentioned in previous posts, I could theoretically “survive” a 7-8 year span without selling any equities. Finally, I’ve not used any 3rd party risk classifications, but it’s certainly a viable consideration as you’re looking at what allocation to include in each bucket. Hope that helps, thanks for stopping by!

Would appreciate your review of Michael McClung’s “Living Off Your Money”. He has a similar approach with some specific guidelines.

Very detailed analysis.

thanks

Bob

Thanks for the tip, Bob. I’ll look it up. Unfortunately, I have too many books in my “to read” pile already, but I’ll get to it in time! Sounds like it’s worth a read, thanks for sharing.

Hello Fritz,

My name is Javier from Spain, and this is the first time I write to you.

I am close to retirement and have discovered a brave new world in your blog and all these retirement methods to make our money last.

Thank you for this labor of love in your blog. I’m really learning a lot.

Now the question I can’t answer myself on the bucket strategy.

Unlesss I am missing some basic concept (which wouldn’t be unlikely) I conclude that either I use the bucket strategy OR I rebalance my portfolio. I can’t have both.

I mean, either

Option 1 I choose an asset allocation (static or dynamic) and stick with it (i,.e. I rebalance periodically my assets), or

Option 2 I hand-pick every year which assets to sell from my portfolio (i.e. the ones with positive returns), hence de-balancing my asset allocation.